Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

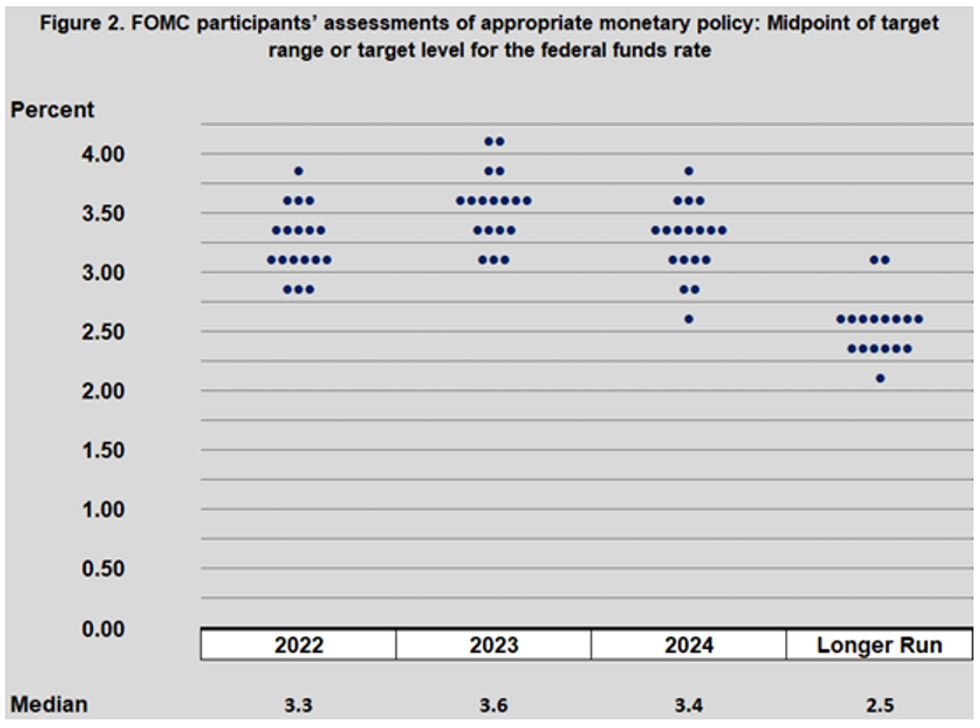

We'd tend to be be a little below consensus on the 2022 median Fed funds dot expectation (which judging from sell-side looks like 3.4%), with a few dots in the 2.75-3.00% range (those on the FOMC who might want to "pause" after aggressive hikes through September), several at 3.00-3.25% (75bp in Jun, 75bp Jul, then 25bp in Sep/Nov/Dec), and several more above that.

- Our end-2022 median of 3.3% splits the difference, with an equal number seeing rates above / below 3.25%.

- Neutral rates are seen at 2.0-3.0% and many FOMC members have wanted to wait and see how the data plays out before committing to aggressive hikes through the rest of the year. And if they go 75bp today and signal a strong hike in July, the ostensible point of front-loading hikes is so that you have the opportunity move less aggressively further down the line.

- For 2023, we'd pencil in another couple of implied hikes in the median (3.6% with risks of 3.9%), then moving lower in 2024. Even in March's SEP, at least two participants pencilled in 2024 rate cuts.

- Then again, the FOMC has pretty much continually surprised us on the upside with their recent dot plots, so take that for what it's worth. We'll certainly be eyeing the dots at the high end of the distribution, as they've been more right than wrong so far.

Source: MNI

Source: MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok