Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China trade figures were weaker than expected from an export and import growth standpoint. Export growth printed at -14.5% y/y, versus -13.2% expected. Imports were -12.4% y/y, versus a -5.6% forecast. Export growth is back to early 2020 levels, while imports are trending back down, although remain above earlier 2023 lows (near -20% y/y). At face value the data suggests the economic backdrop remains a challenging one.

- One positive from a CNH perspective is a largely than expected trade surplus for July, coming in at $80.6bn, versus $70bn forecast.

- The reaction in USD/CNH has been fairly muted so far. We did spike a little higher, but now sit back closer to 7.2200. As we noted earlier, the extent to which the CNY NEER has already fallen in recent months has discounted a weaker export growth backdrop, see the first chart below.

- Processing exports (with imported materials) continued to ease, down -22.1% y/y from -19.5% in June.

Fig 1: China Export Growth & CNY NEER Y/Y

Source: MNI - Market News/Bloomberg

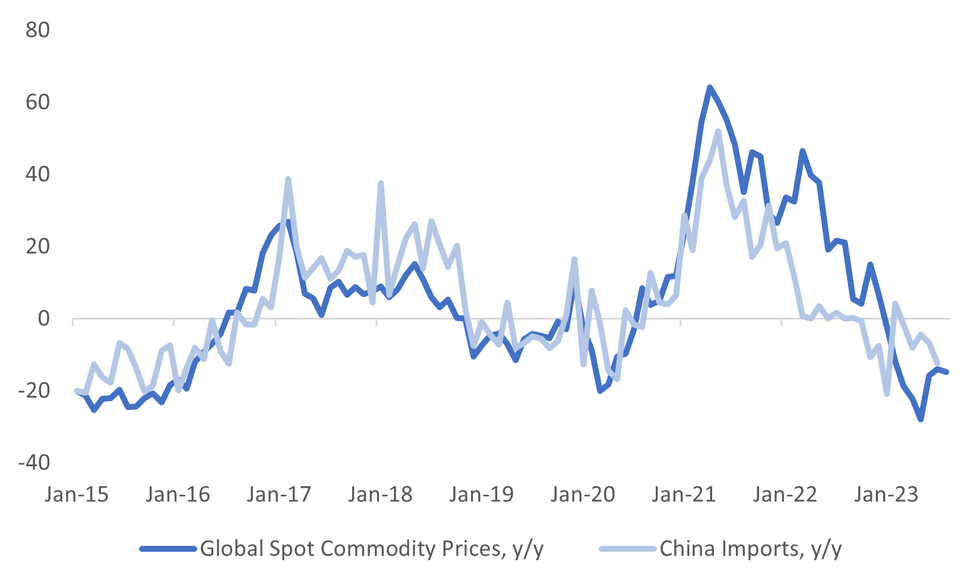

- On the import side, the weaker than expected result shouldn't add to the recovery in aggregate commodity prices in recent months (albeit still negative in y/y terms), see the second chart below.

- Iron ore and oil imports were down in volume terms for July versus June, but still up in y/y terms, more so for oil. Coal import volumes were also down a touch in m/m terms, but like oil up comfortably versus levels from a year ago.

Fig 2: China Imports & Aggregate Commodity Prices Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok