Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

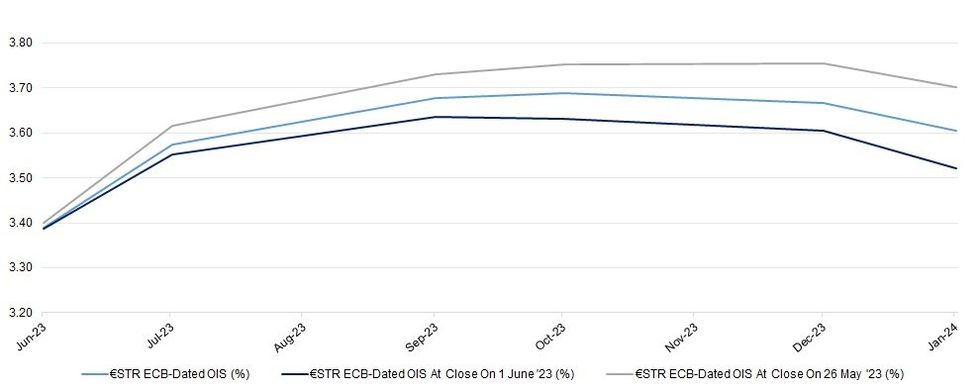

Yesterday’s ECB consumer inflation expectations survey-inspired tick lower in ECB-dated OIS pricing consolidates, even with crude oil futures rebounding from Tuesday’s worst levels (EUR 5y/5y inflation linked swaps have moved back above 2.50%, just, after their limited foray below yesterday).

- That leaves broader ECB pricing in familiar territory, with terminal pricing currently residing in the 3.75-3.80% window (in deposit rate terms).

- Executive Board member Schnabel has once again stressed that underlying inflation remains “high,” with a peak in underlying inflation not deemed enough when it comes to declaring ‘victory.’ She also highlighted the Bank’s data-dependent stance.

- ECB speak will headline the regional docket today, with de Guindos, Panetta, Knot and Vujcic all slated. All of those individuals have spoken within the last week or so, perhaps limiting the scope for meaningful market impact.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jun-23 | 3.389 | +24.4 |

| Jul-23 | 3.575 | +43.0 |

| Sep-23 | 3.678 | +53.3 |

| Oct-23 | 3.688 | +54.3 |

| Dec-23 | 3.666 | +52.1 |

| Jan-24 | 3.604 | +45.9 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok