Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

1 month USD/KRW surged from the low 1370 region to just shy of 1395 post the stronger than expected US CPI print (we ended NY at 1391.40). This is fresh cyclical highs in the pair going back to 2009. Onshore spot closed yesterday at 1373.85, so expect some catch up in onshore markets.

- The early focus will be the extent to which officials push back on fresh highs in USD/KRW. Rhetoric has stepped up in recent weeks, and a quick break through 1400 may be seen as undesirable.

- Still, given broad based USD strength, fresh cyclical highs in UST yields (nominal and real), there may not be much the authorities can do in the near term.

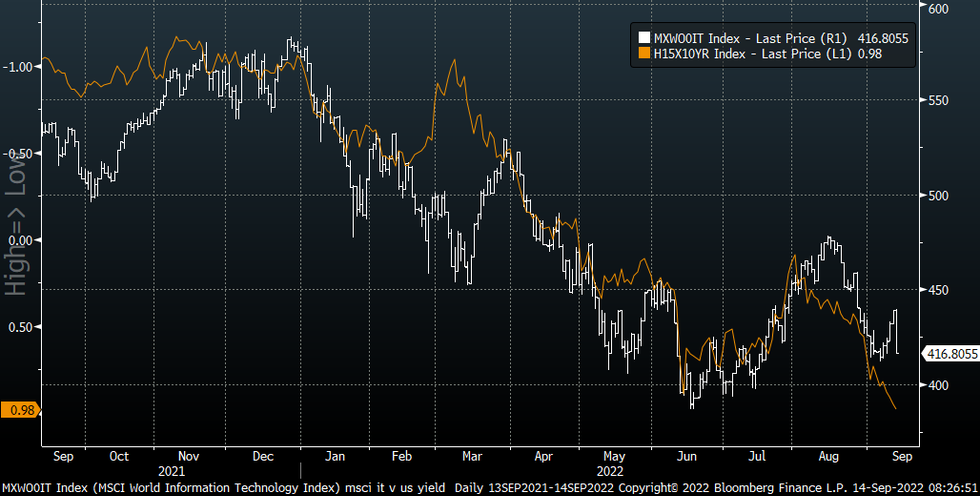

- We are also mindful of negative spill over from USD/CNH, which is back close to 7.00 (last 6.9830), and equity market weakness. The chart below overlays the US real 10yr yield against the MSCI IT index. Note the US real yield is inverted on the chart

- The domestic data calendar is empty today.

Fig 1: US Real Yield & MSCI IT

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok