Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

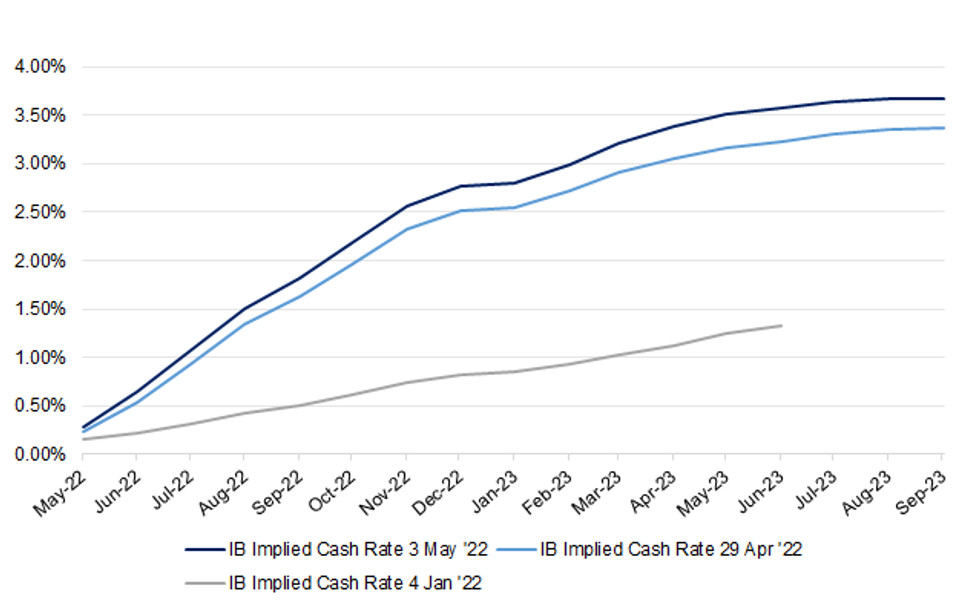

Market pricing provides a more hawkish view than several points of reference that the RBA disclosed, with cash rate expectations, as viewed via Tuesday’s IB strip settlement levels, ratcheting higher post-decision, leaving terminal cash rate expectations above 3.50%. For reference, the Bank revealed that its new round of economic forecasts is based on a year-end cash rate of 1.50-1.75%, with Governor Lowe pointing to a more “normal” level of interest rates being ~2.50%. Market pricing still looks very aggressive in this context, but as we have noted previously, this doesn’t mean that there is an obvious trigger point to trigger receive side interest.

- Yesterday’s settlement levels pointed to a year end cash rate of 2.75%, 240bp above the current cash rate target. With only 7 meetings left in ’22 that eqates to over 30bp of tightening per meeting, on average.

- Governor Lowe suggested that the 25bp hike was a case of “business as usual,” although most of the sell-side have touched on the potential for a 40bp hike, perhaps as soon as June, which would move the cash rate target back to the traditional 25bp multiples and fully reverse the emergency cuts provided in March 2020. The RBA now has ample time to provide intra-meeting messaging if it so chooses.

- Some sell-side names remain cognisant of the potential for the level of household debt to cap the terminal rate in the high 1s or low 2s. Past RBA research has pointed to most households being able to cope with 200bp of tightening and Governor Lowe’s rhetoric suggests that the RBA will look to push past the lower end of the current terminal rate expectations, if given the chance.

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.