Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

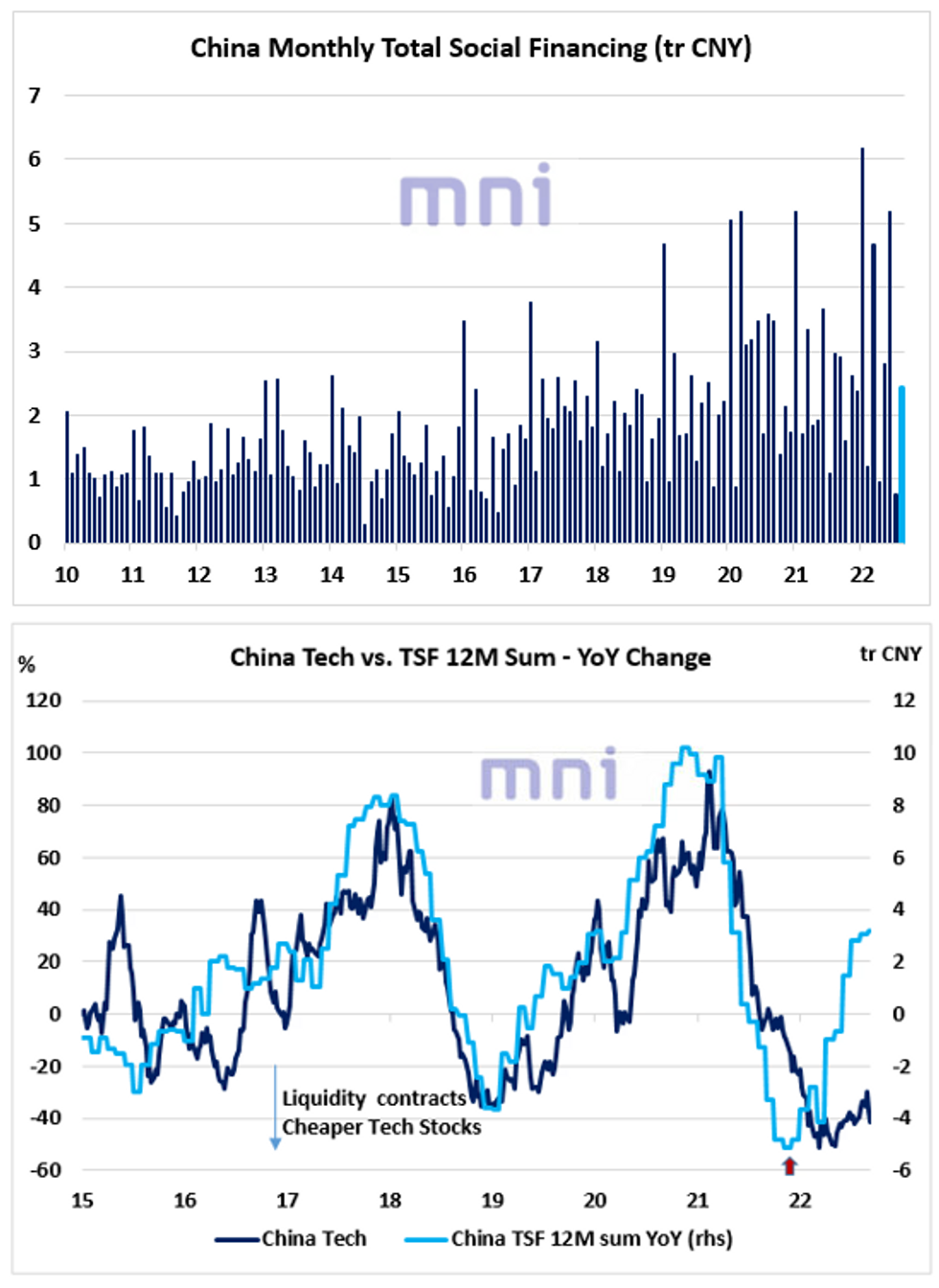

- The PBoC reported this morning that aggregate financing rose by 2.43tr CNY in August, above expectations of 2.075tr CNY with new yuan loans rising by 1.25tr CNY (1.5tr CNY exp.).

- China ‘liquidity’ metric, computed as the annual change in China Total Social Financing (TSF), continues to rise, now up 3tr USD in the past year.

- Even though a recovery in liquidity has historically had a positive impact on domestic risky assets and some China-sensitive commodities (i.e. copper) or currencies (i.e. AUD), the easing conditions (policy and liquidity) have been barely enough to limit the downside risk on the real economy.

- The bottom chart shows that liquidity-sensitive sectors such as tech equities have remained 'depressed' despite the sharp rebound in liquidity since the start of the year.

- Sell-side firms have been constantly reviewed their 2022 forecasts to the downside, with some analysts expecting GDP growth to average 2.5%-3% this year, diverging significantly from China officials 5.5% growth target.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok