Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BUNDS

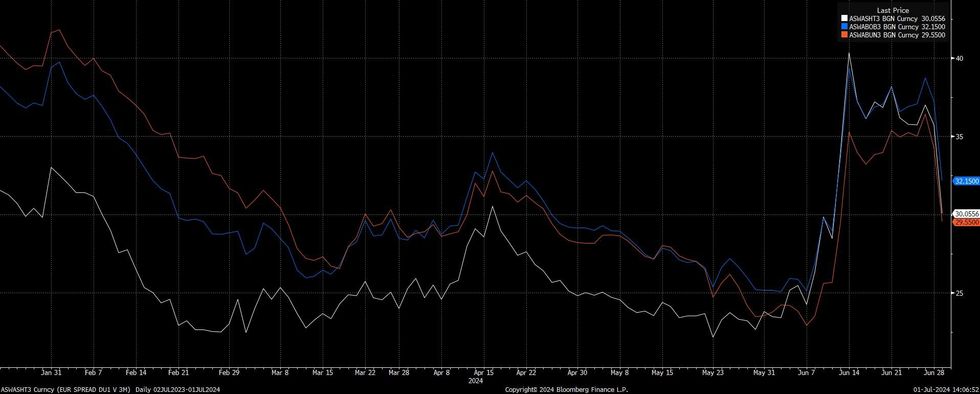

Most of the major German ASW spreads still sit comfortably wider vs. pre-snap election announcement levels, meaning that at least some French political risk premium remains in place, consistent with wider cross-market pricing.

- While most deem it unlikely that RN will achieve an absolute majority come the end of the second round of voting, questions surrounding political paralysis and the lack of ability to crimp fiscal spending are limiting spreads from tightening further.

- Schatz ASWs have led today's tightening, which is understandable given the relative sensitivities to the French uncertainty seen since the start of June.

- Late Friday saw Morgan Stanley recommend a Bobl/Buxl ASW box flattener, which is now a little offside. Note this was a short-term trade, which they suggested “should provide a near-term risk-off hedge in the event of an adverse outcome in the French elections, with limited downside.”

- Looking ahead, Goldman Sachs point towards an eventual re-tightening in Bund ASWs. Late on Friday they noted that “Bunds have emerged as clear beneficiaries of renewed sovereign risk. This suggests to us that there is better risk reward in ASW tighteners as a means to fade French election risk premium.”

- They concluded that the pre-election move in Bund ASWs was “overdone, and likely reflects positioning following the strong tightening trend of the last year.”

- We flagged this positioning element on several occasions during the initial ASW widening episodes in early June.

Fig. 1: Schatz, Bobl & Bund ASWs Vs. 3-Month Euribor

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok