Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

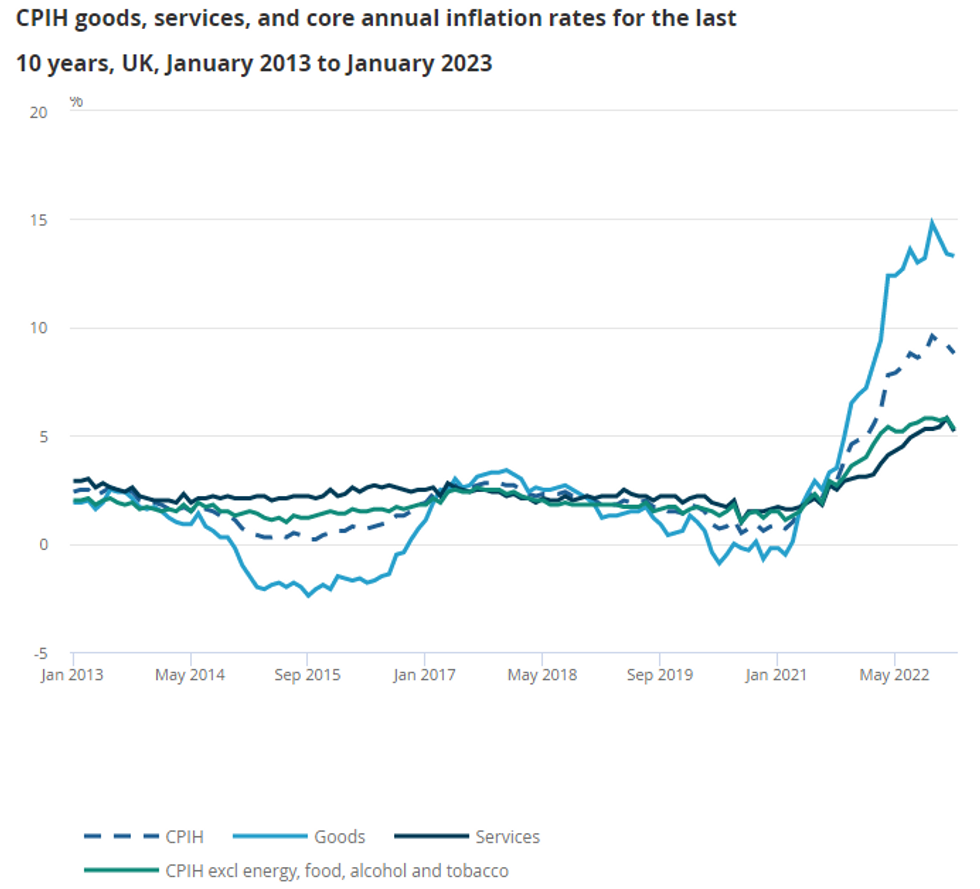

UK JAN CPI -0.6% M/M (FCST -0.4%); DEC +0.4% M/M

UK JAN CPI +10.1% Y/Y (FCST +10.3%); DEC +10.5% Y/Y

UK JAN CORE CPI -0.9% M/M, +5.8% Y/Y (FCST +6.2%); DEC +6.3% Y/Y

- The January inflation data for the UK saw downside surprises as prices declined -0.6% m/m, easing 0.4pp to +10.1% y/y.

- Transport was the key downwards driver in January, down -3.6% m/m alone and decelerating from +6.5% y/y in December to +3.1% y/y. The reversal of the December spike in airfares was the key driver.

- Core inflation fell -0.9% m/m, cooling 0.5pp to +5.8% y/y, the lowest since June 2021. Services inflation slowed by 0.8pp to +6.0% y/y, largely driving the lower headline print. This was again largely due to transport passenger services, and to a lesser extent restaurants and cultural services.

- This data implements the new 2023 expenditure weights. According to an ONS spokesperson, airfare weights increased over a threefold, contributing to the marked downwards effect on headline CPI and to a lesser extent the increased weighting of accommodation services.

- As such, the fall in the MPC's closely watched core-reading will likely be taken with a grain of salt, especially following yesterday's uptick in wages. However, the data confirms inflation is moving in the right direction.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok