Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China November inflation data was close to expectations. Headline CPI printed at 1.6% y/y, in line with expectations and versus 2.1% in October. PPI was slightly better, relative to forecasts, coming in at -1.3% y/y, against -1.5% expected.

- For the CPI, the m/m fell by -0.2%, as food prices stepped back to a 3.7% y/y pace from 7.0% last month. Non-food inflation remained very benign at 1.1% y/y, unchanged in the month while core (ex food and energy) was also unchanged at 0.60% y/y. 3 out of the 8 sub-indices recorded faster y/y momentum in November, versus just 1 in October.

- For the PPI, outside of consumer goods (+2.0% y/y), falls were recorded for mining (-3.9%), and manufacturing (-3.2%), albeit at a reduced pace compared to last month.

- Close to expectations for these prints has limited the market reaction, with markets also remaining forward looking around the re-opening theme.

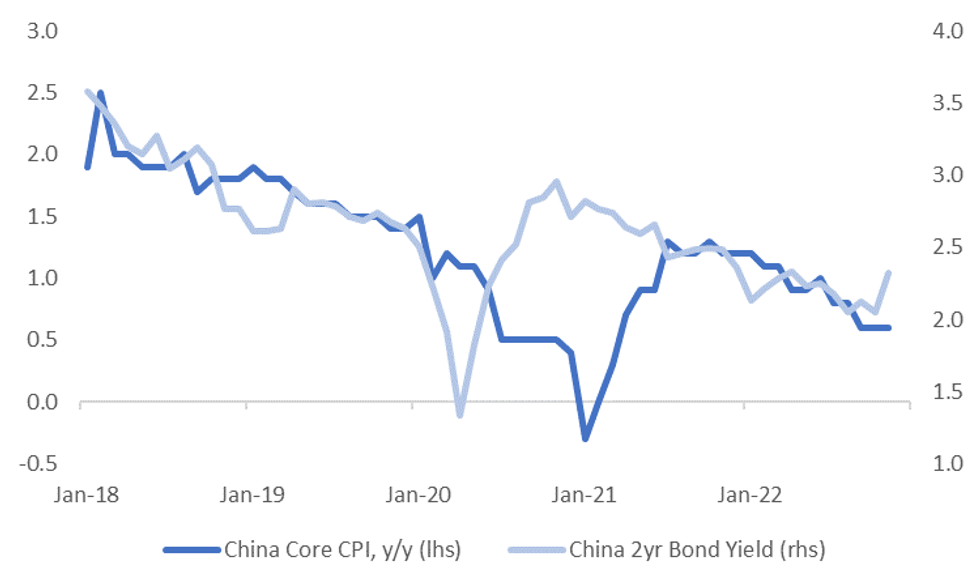

- China government bond yields have diverged somewhat from the continued soft pace in terms of core inflation, see the chart below.

Fig 1: China Core Inflation & 2yr Government Bond Yield

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok