Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS/SUPPLY

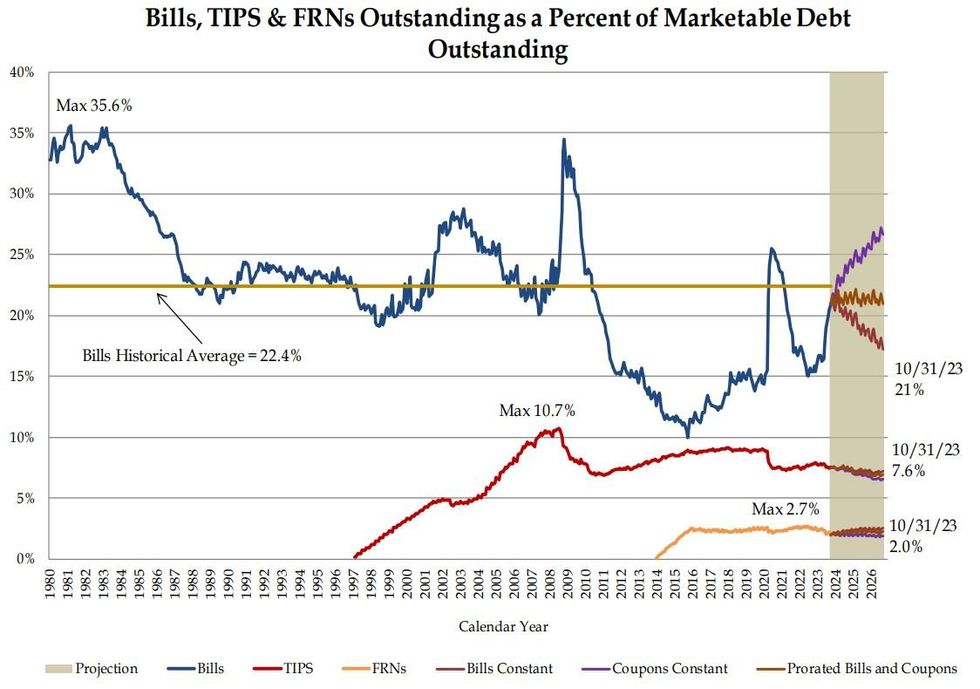

Bills and buybacks were also an area of focus for this announcement:

- On bill issuance: TBAC recommended net bill issuance for Q4 (Oct-Dec) of $437.45B (this is basically an imputed figure: $776B, the figure in Monday's borrowing requirement doc for Q4, minus $338.55B in net bond issuance). TBAC bills recommended for Q1 (Jan-Mar) is $467.60B, which added to $348.40B in net bond issuance = $816B marketable borrowing requirement.

- These bill estimates will be roughly line with Treasury's which as noted have announced slightly smaller 10s / 30s auctions than TBAC recommended for the upcoming quarters but larger FRNs (TIPS upsizing was in line).

- This is a of course a slowdown by comparison to the post-debt limit cash buildup which will have seen a staggering $1.5T in net bill issuance since early June.

- Treasury notes "By early-December, Treasury anticipates implementing modest reductions to short-dated bill auction sizes that will likely then be maintained through mid- to late-January." That's largely as expected.

- This still will mean bills as a % of marketable debt will remain well above the 20% upper TBAC-recommended threshold, though TBAC reiterated "continued comfort with the bill share of total marketable debt outstanding remaining temporarily above its recommended range given continued robust demand for bills and Treasury’s regular and predictable approach."

- In a minor surprise, 6-week bills weren't made a benchmark (Treasury is "actively evaluating" this), despite TBAC noting primary dealers' "near unanimous support for converting the 6-week cash management bill to a benchmark tenor." Treasury will continue to issue 6-week bills at least through March 2024.

- On buybacks: "Treasury intends to provide an update on the timing for implementing the regular buyback program in the next quarterly refunding announcement." We interpret this as a signal that it's likely on Jan 31 they'll be announcing the start of the program - as expected.

Source US Treasury Quarterly Refunding Announcement

Source US Treasury Quarterly Refunding Announcement

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok