Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

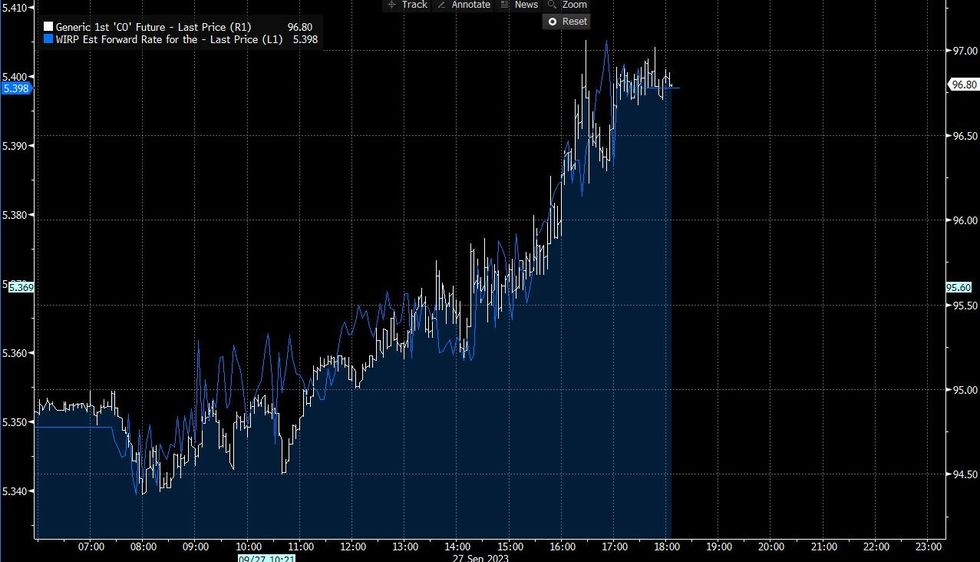

- BoE peak rate pricing picked up 4bp Wednesday to the highest since the the MPC hold on the 21st, with 21bp of further hikes implied to a 5.46% Bank Rate. Though there were no specific catalysts for the move, the rise in implied tracked a weaker GBP and rising oil prices in lockstep intraday. There's 10bp of hikes priced for the Nov 2023 meeting (40% probability of a 25bp hike). Cut pricing fell back sharply, with 73bp of reductions expected in the year following the peak in Mar 2024, vs 80bp at Tuesday's close (and the fewest implied cuts in 2 weeks).

- ECB terminal depo rate pricing was unchanged at 4.05% (5bp of hikes from current levels), with still virtually no chance seen of a hike at the next meeting in October, as we head into the September flash inflation round starting first thing Thursday. There's around 60bp of cuts priced between the end of the tightening cycle in Dec 2023 and end-2024, having been in a range of 60-70bp since late August.

Oil Prices And March 2024 OIS Implied PricingSource: BBG, MNI

Oil Prices And March 2024 OIS Implied PricingSource: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok