Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI View:

After extending QE by GBP100bln in June, immediate changes to policy are unlikely at this meeting but the tone for the next three months at least is likely to be set at this meeting. There will be three main areas of discussion as the decision and MPR is initially released:

- How have the banks views on the economic outlook changed and has the MPC been able to come to enough agreement to publish a full projection with fan charts? We think multiple scenarios are more likely.

- Is there any update on the review of the effective lower bound (ELB) and negative rates? We think the review will be released later in the year and think that the Bank will not rule out the use of negative rates but could say that negative rates are not an active policy instrument until the completion of the review.

- What will happen to the pace of QE? We expect the pace to fall to around GBP800mln per operation (GBP4.8bln per week, down from GBP6.9bln).

- The final consideration will not come until the embargoed press Q&As which are due for release at 10:00BST. This concerns the sequencing of how the Bank will eventually remove stimulus – does the MPC plan to raise interest rates first or reduce the size of its balance sheet?

This is our most comprehensive BOE preview to date and new for this month includes a section summarising speeches from MPC members since the last meeting.

Click the link below for the full BOE preview:

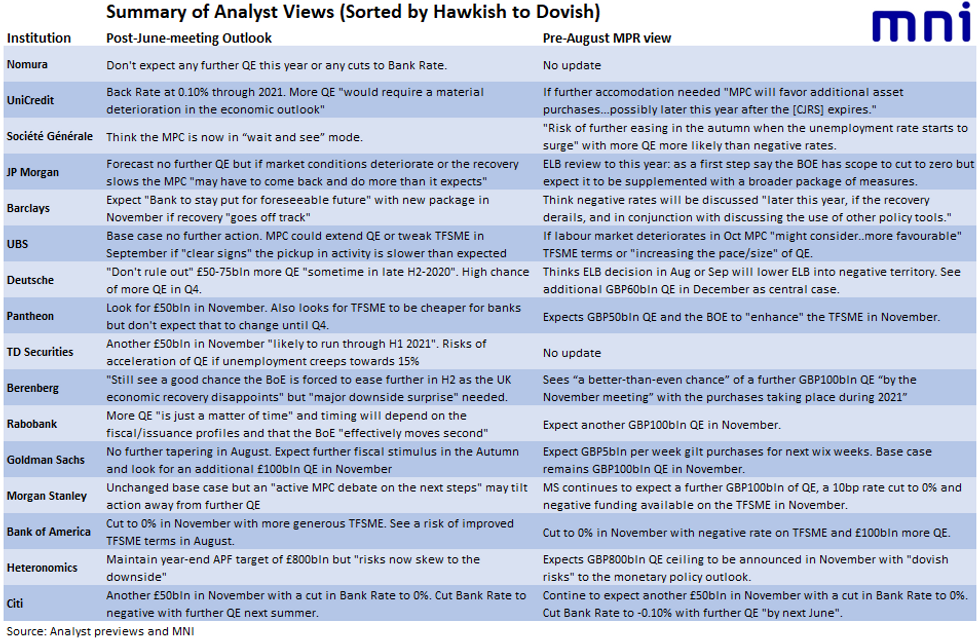

Sell side BOE Expectations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok