Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

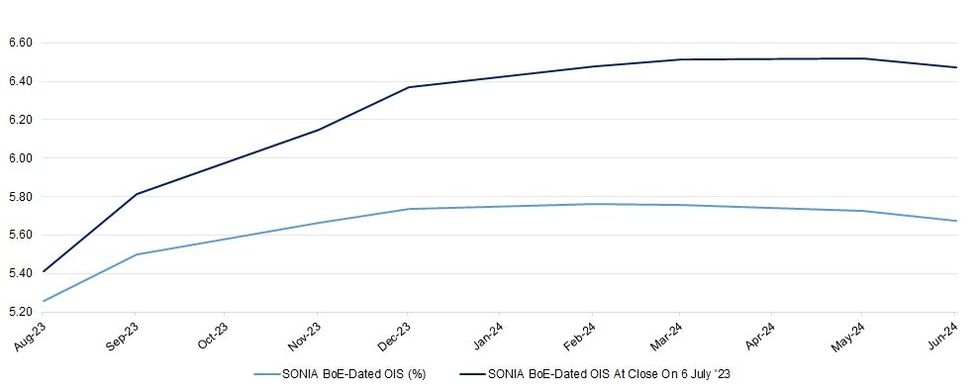

A little more colour when it comes to the previously outlined moves away from early July hawkish extremes in BoE-dated OIS pricing after the recent run of tier 1 domestic data facilitated a meaningful pullback in pricing. The contract covering today’s meeting shows around 32.5bp of tightening priced, a little over 15bp shy of the most hawkish closing levels witnessed in early July, while terminal policy rate pricing has eased by ~75bp (also based on closing levels) over that horizon, to stand just below 5.85%, as well as rolling forwards to the February MPC from the May MPC. Intraday highs were more pronounced than closing levels, but markets were particularly thin at that time, so we have marked the moves against the closes.

| BoE Meeting | SONIA BoE-Dated OIS (%) | SONIA BoE-Dated OIS At Close On 6 July '23 |

| Aug-23 | 5.257 | 5.413 |

| Sep-23 | 5.501 | 5.812 |

| Nov-23 | 5.662 | 6.148 |

| Dec-23 | 5.735 | 6.369 |

| Feb-24 | 5.762 | 6.479 |

| Mar-24 | 5.757 | 6.513 |

| May-24 | 5.725 | 6.518 |

| Jun-24 | 5.676 | 6.475 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.