Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EMERGING MARKETS

- Selling pressure has been surging in Hungarian risky assets following Orban's tax plan, which will use emergency measures for a Ukraine crisis windfall tax on large companies.

- Hungarian equities fell below the March lows yesterday before consolidating higher; the BUX index is still down nearly 30% since its January high.

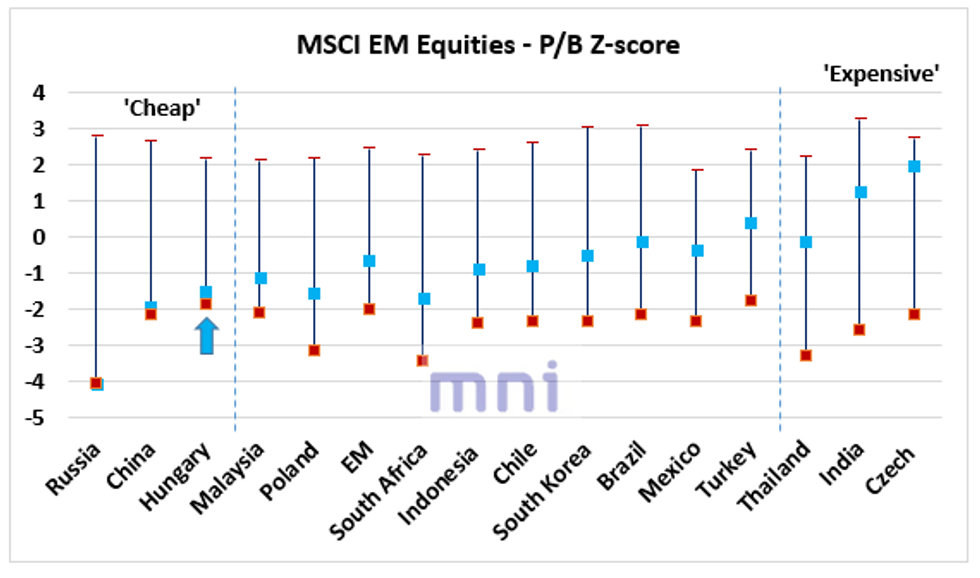

- Hungarian equity market is now the second cheapest among the EM world following the recent selloff, and the current climate (i.e. geopolitical uncertainty, stagflation risks) leaves domestic risky assets vulnerable in the short run.

- China equities remain the ‘cheapest’ EM equity markets (excluding Russia from ranking) as zero-Covid policy continues to weigh on the real economy and domestic risky assets.

- Easing signals from China officials combined with the rebound in 'liquidity' (TSF 12M Sum) in recent months have not been enough to stimulate risky assets, which continue to trade at low levels relative to historical standards.

- Momentum on the Hang Seng Index remains bearish in the near term; the index is down nearly 20% since its January high and down 35% since its February 2021 peak.

- In this chart, we compute the z-score of P/B ratios of the 16 EM equity markets (15 countries + MSCI Emerging Market index) using over 10 years of data (starting January 2010) and then rank them from 'cheapest' to 'most expensive' based on the distance between the minimum value and the current z-score.

- At the top, Czech is the 'most expensive' market among the EM world, with a current price-to-book ratio of 2.13 (vs. 1.48 for EM MSCI index).

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok