Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

China's data calendar swings back into gear tomorrow. PPI and CPI prints are out for June. PPI is expected to ease to 6.0% from 6.4%, but CPI is forecast to rise to 2.4%, versus 2.1% previously. There is some chatter of a potentially higher CPI print due to rising food prices. The authorities have steeped in to curb pork prices rises this week.

- Beyond that, from Monday onwards aggregate financing and new loans for June are also due. Further gains are expected in both prints (aggregate finance to 4200bn yuan versus 2792.1bn previously, and new loans to 2400bn yuan from 1883.6bn yuan).

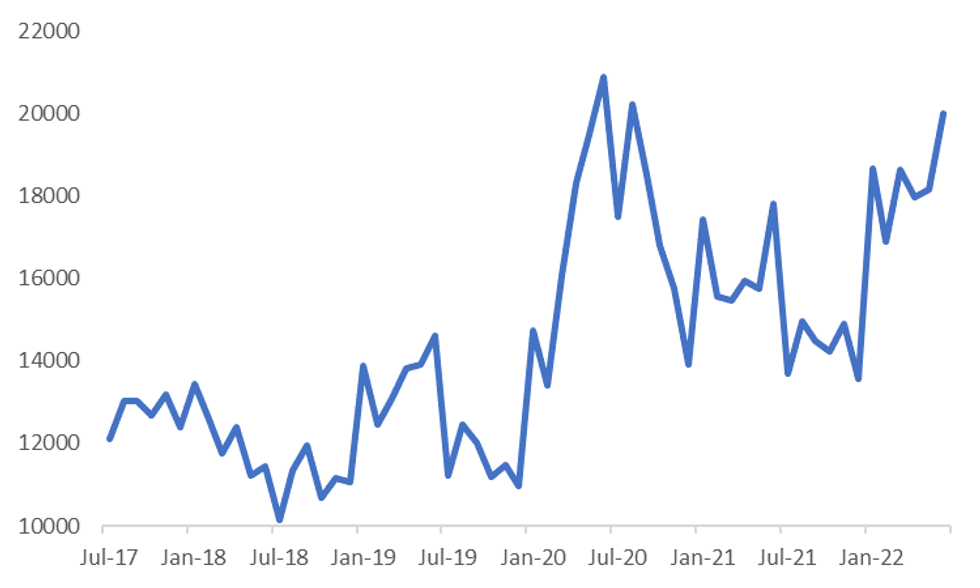

- If the projected increase in aggregate finance is realized it would push the rolling 6 month sum of financing activity back close to 2020 highs, see the chart below.

Fig 1: China Aggregate Finance - 6 Month Sum (Assumes June Consensus Forecast Is Realized)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

- On Wednesday trade figures are due for June. The market expects export and import growth to ease slightly (12.9%yoy from 16.9% for exports and 4.0% from 4.1% for imports). The trade surplus is forecast to remain strong at $76.80bn, versus $78.76bn last month.

- From Wednesday onwards we may also have the 1-yr MLF lending decision. No change is expected at 2.85%.

- On Friday, we get the monthly data run for June. IP and retail sales are expected to improve further, but fixed asset investment is forecast to moderate.

- The same day also delivers Q2 GDP, which is expected to contract by -2.3% in QoQ terms, bringing YoY growth down to 1.0% from 4.8% in Q1. These numbers may be revised as more forecasts are submitted to Bloomberg.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok