Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

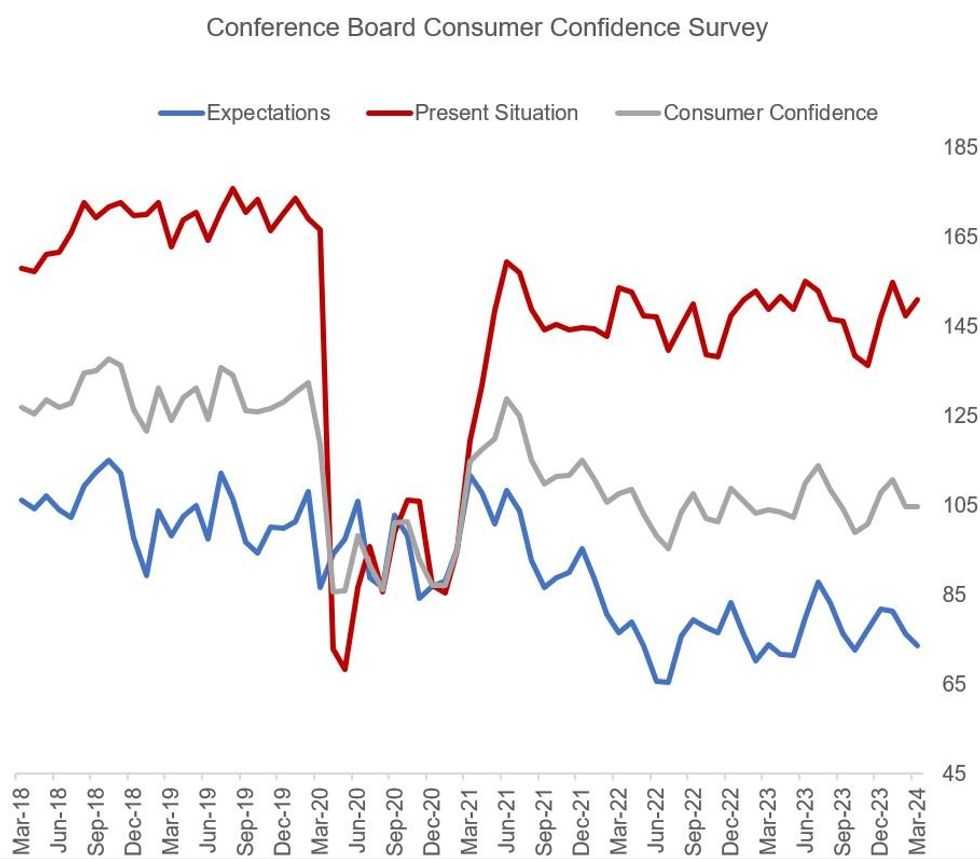

March's Conference Board consumer survey showed an unexpected fall in confidence, including a downward revision to February's reading. While expectations also retreated, the "present situation" component picked up. The internals of the report were fairly weak, with inflation apparently remaining front-of-mind for many respondents. In general the survey readings have been fairly steady since early 2022, consistent with the roughly 2% annual average real personal consumption growth posted over that span.

- The Consumer Confidence index dipped from 104.8 to 104.7, defying expectations of a rise to 107.0 (prior was revised down from 106.7). Present Situation rose from 147.6 (rev. from 147.2) to 151.0, with Expectations slipping from 76.3 (rev. from 79.8) to 73.8.

- Average 12-month inflation expectations were 5.3% (little changed from 5.2% prior), while recession fears continued to fade.

- Consumers had a weaker assessment of current business conditions in March, and were more pessimistic on the outlook for short-term business conditions, the labor market, and their short-term income prospects. However they had a more optimistic assessment of the current labor market. A few interesting observations from the report:

- "Consumers remained concerned with elevated price levels, which predominated write-in responses...over the last six months, confidence has been moving sideways with no real trend to the upside or downside either by income or age group.”

- "Notably, the employment differential—those saying jobs are plentiful minus those saying jobs are hard to get—rose in March and has been trending higher this year. However, expectations for the next six months slipped to the lowest level since October 2023."

- "The share of consumers expecting an increase in interest rates over the year ahead rose above 50 percent for the first time since November 2023."

- "On a six-month basis, buying plans for interest-rate sensitive items like autos, homes, and big-ticket appliances dipped again. However, based on a supplemental question, planned spending for services in 2024 increased relative to the same time last year."

Source: Conference Board, MNI

Source: Conference Board, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok