Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORWAY

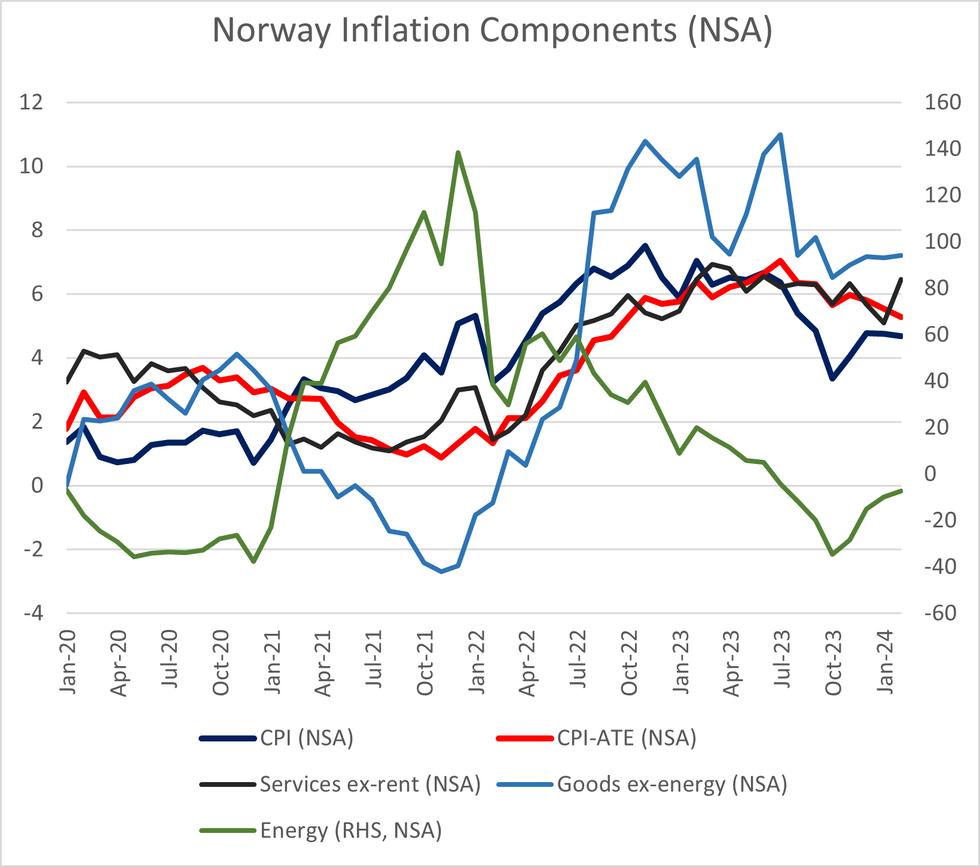

Norway January CPI-ATE printed in line with consensus on an annual basis (5.3% Y/Y vs 5.5% prior), while the NSA monthly rate was a touch firmer than expected at 0.0% M/M (vs -0.1% cons, 0.2% prior). Norges Bank had forecasted 5.4% Y/Y in the December MPR. Overall, there was a broad-based acceleration in the annual rate of core components. EURNOK traded 17 ticks lower on release but has since pared losses.

- A reminder that domestic analysts generally saw CPI-ATE below 5.3% Y/Y, driven by a larger than expected deceleration in food prices in January. Food prices were 8.7% Y/Y (vs 8.9% prior) and 1.4% M/M (vs -2.0% M/M prior).

- Looking at the break-down of the main subcomponents, both services-ex rent (6.5% Y/Y vs 5.1% prior) and Norwegian goods ex-energy (7.2% Y/Y vs 7.1% prior) accelerated on an annual basis in January. Within services, the restaurant/hotels and recreation/culture components rose on an annual basis, with a deceleration in transport prices not enough to offset.

- At a more granular level, Statistics Norway's measure of services where labour inputs dominate rose to 3.8% Y/Y (vs 2.4% prior), the highest rate since May 2023.

- Within core goods, clothing/footwear prices also accelerated. The "Miscellaneous goods and services" component (less than 10% weight in the index) rose 3.8% Y/Y (vs 1.4% prior). We note this appears to be driven by the "other services " sub-component, which rose 8.7% Y/Y (vs 0.7% prior).

- Headline inflation was higher-than-consensus at 4.7% Y/Y (vs 4.6% cons, 4.8% prior) and 0.1% M/M (vs 0.0% cons, 0.1% prior), as energy base effects moderated (energy inflation was -7.2% Y/Y vs -9.8% prior). Norges Bank had forecasted 4.8% in the December MPR.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok