Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

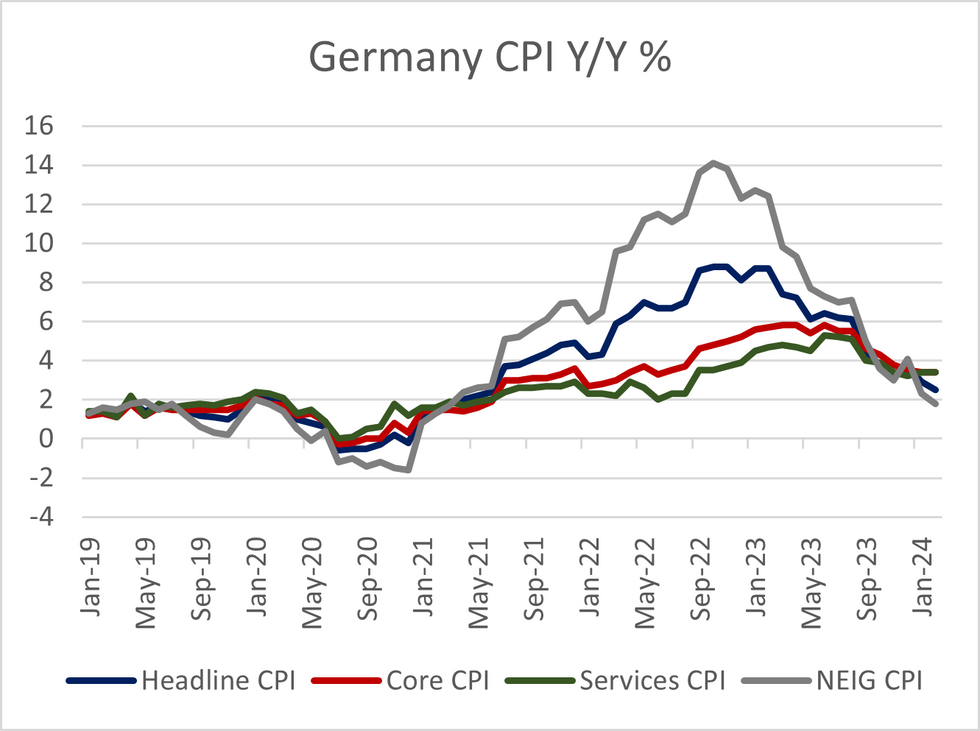

German national flash February core CPI inflation was 3.4% Y/Y, steady versus January's print and a touch below MNI's tracking of 3.5% following the state-level data earlier this morning.

- Services printed at 3.4% Y/Y (unchanged vs the January print). A possible reason for the stalling in services inflation, per Goldman Sachs ahead of the release, are that effects from Germany's restaurant VAT rise are still being fed-through to end prices with a delay. While we'll have to wait for the final report for a breakdown, MNI's estimate for "Restaurants and hotels" inflation suggested no change from the 6.3% Y/Y run rate in January.

- Core goods disinflated to 1.8% Y/Y (vs 2.3% prior), as widely expected.

- Headline CPI was 2.5% Y/Y, below the 2.6% we had tracked from the state-level data this morning and what consensus was expecting coming into the release.

- Food CPI decelerated markedly to 0.9% Y/Y (vs 3.8% prior) while energy still had a dragging effect at -2.4% Y/Y (vs -2.8% prior).

- Headline HICP was in line with consensus at 2.7% Y/Y and 0.6% M/M (vs 3.1% Y/Y and -0.2% M/M prior).

- Taken alongside the French and Spanish prints this morning, the overall Eurozone HICP figure appears to be tracking in line/a touch firmer than the 2.5% Y/Y consensus, with the core HICP expectation of 2.9% Y/Y potentially subject to upside risks (though it's not a straightforward translation from CPI to HICP).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok