Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA DATA

China headline inflation printed as expected at 0.2% y/y. We were down -0.2% in m/m terms, the fourth straight m/m fall. Consumer goods fell -0.3%, (-0.4% prior), while services inflation eased to 0.9% (1.0% prior). Non-food inflation was flat, while the ex food and energy core measure was 0.6% y/y, versus 0.7% prior.

- Looking at the sub-categories, only food and medical care recorded firmer y/y momentum versus Apr. The 6 other sub-categories saw either the same y/y pace or a deceleration.

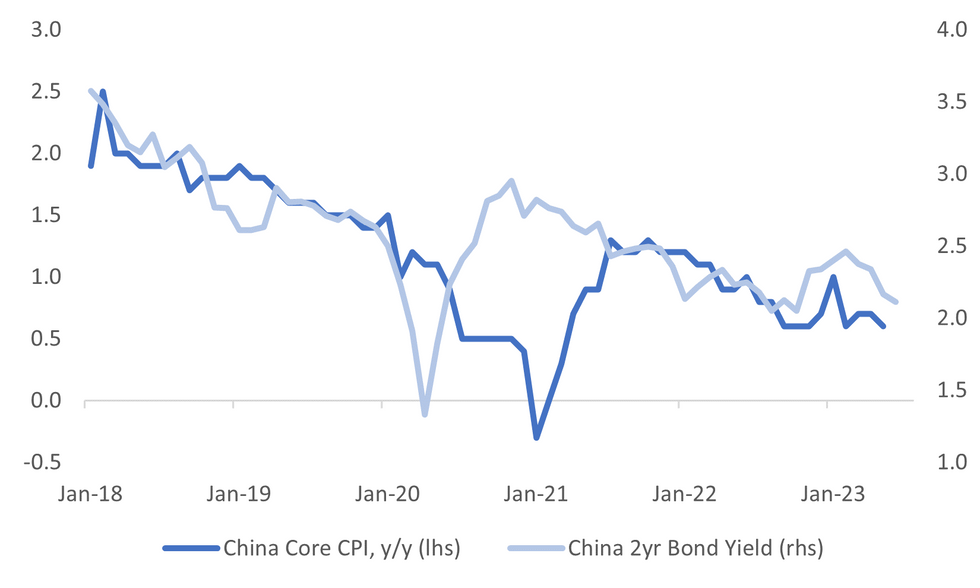

- The first chart below overlays the core CPI and 2yr government bond yield. Core inflation is back to recent cyclical lows, which coupled with weaker m/m headline momentum is likely to keep easing calls still part of the market narrative.

Fig 1: China Core Inflation & 2yr Government Bond Yield

Source: MNI - Market News/Bloomberg

- On the PPI side, the headline -4.6% was the weakest y/y print since 2016. Mining was -11.5%y/y, raw materials -7.7% y/y, with both in line softer global commodity prices in recent months.

- Manufacturing PPI slipped further into contraction though, -4.6% y/y (from -3.6%), while consumer goods were -0.1%y/y, led by consumer durables at -1.1% y/y. Both measures are back to 2021 Q2 lows.

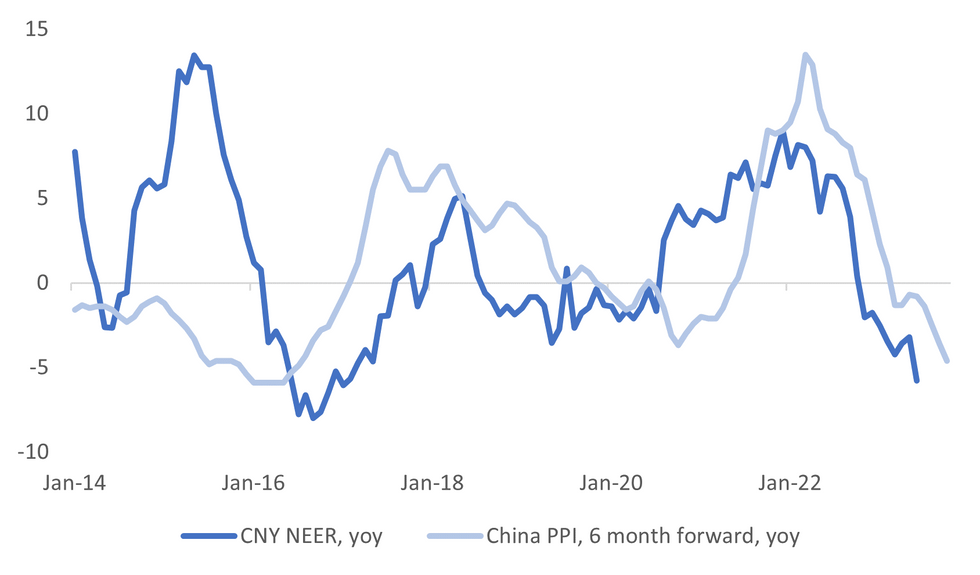

- The second chart overlays the headline PPI y/y against the J.P. Morgan CNY NEER y/y. NEER weakness looks to be running a little ahead of PPI trend, but it is hard to argue there were positives for the CNY FX in today's data.

Fig 2: China PPI Y/Y & CNY NEER Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok