Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

AUSTRALIA DATA

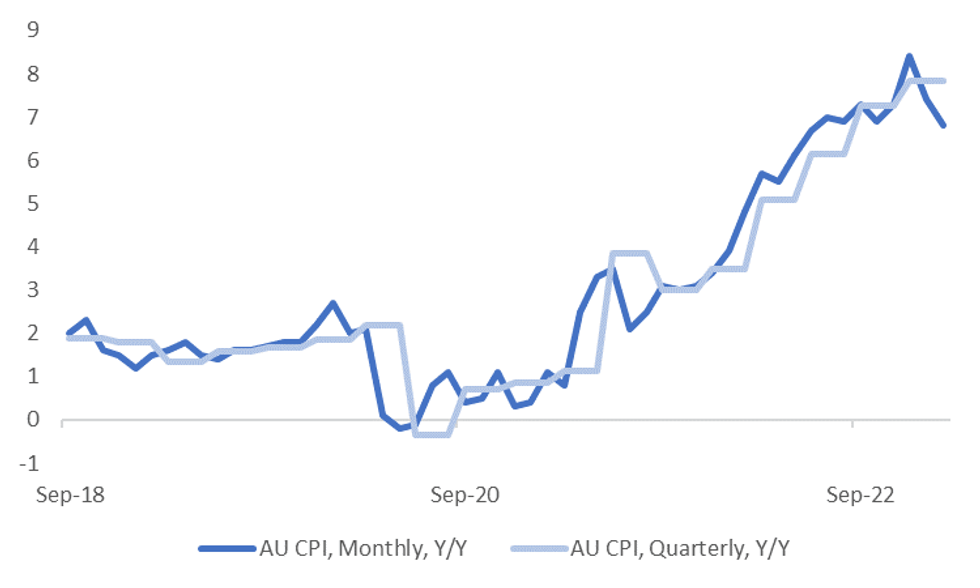

Feb Australian CPI saw a decent downside miss, printing at 6.8% y/y, versus 7.2% y/y forecast and 7.4% prior. Today's outcome is a decent down step from the recent peak of 8.4% recorded in December last year. At face value this it suggests we should see y/y momentum in the quarterly series ease, see the chart below.

- The ABS's measure which excludes volatile items (fruit and vegetables and automotive fuel) fell to 6.9% y/y from 7.5% in Dec. The ABS also noted that a measure excluding holiday and accommodation eased to 6.6% y/y from 6.8%.

- This travel related sub component, recreation, saw the biggest down step in y/y momentum to 6.4% y/y from 10.2%.

- Other sub categories were mixed, but recent inflation pressure points like food and housing recorded lower y/y momentum compared to January.

- Today's result, coupled with yesterday's as expected retail spending outcome, should be enough to offset the resilient business survey backdrop and strong jobs data in terms of next week's RBA decision. All in all, today's data supports the case for a pause next week.

Fig 1: AU CPI Y/Y Momentum Looks To Have Peaked

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok