Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US

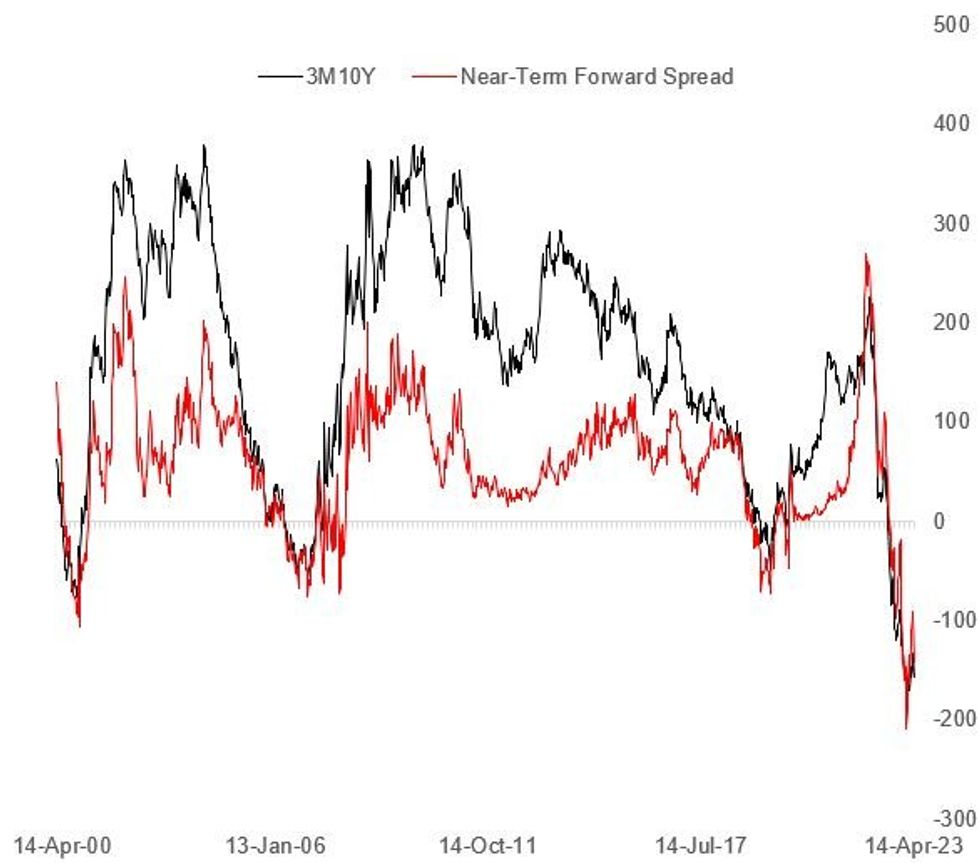

There's been a lot of interest in the economic signals provided by the US yield curve since yesterday's CPI reading has spurred deeper inversions. There are two segments of the curve that probably carry the most weight with respect to "forecasting" recessions: the (Fed-endorsed) near-term forward spread, and the 3 month - 10Y Treasury yield spread. It's worth noting that both are off the most inverted levels of the cycle, but have headed sharply lower after CPI.

- The near-term forward spread is highlighted by Fed staffers as providing "a demonstrably cleaner signal of recessions" than other segments of the curve (2s10s for instance). It's defined as the 3-month Treasury rate 6 quarters forward, vs the 3M treasury yield. But they caution that no matter which curve inversion you look at, "it is not valid to interpret inverted term spreads as independent measures of impending recession. They largely reflect the expectations of market participants."

- In early 2022, Fed Chair Powell played up this measure's explanatory power, and saying “If it’s inverted, that means the Fed’s going to cut, which means the economy is weak." He elaborated on this in November, back before it was inverted: "that’s been our preferred measure. We think, just empirically, it dominates the ones that people tend to look at, which is 2s, 10s, and things like that. So it’s not inverted...if you’re in a situation where the markets are pricing in significant declines in inflation, that’s going to affect the forward curve."

- A week later, this inverted for the first time in the cycle - it now stands at -143bp, vs the -222bp low set in early May, but 60bp lower in the past week.

Source: BBG, Fed, MNI Calculations

Source: BBG, Fed, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok