Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

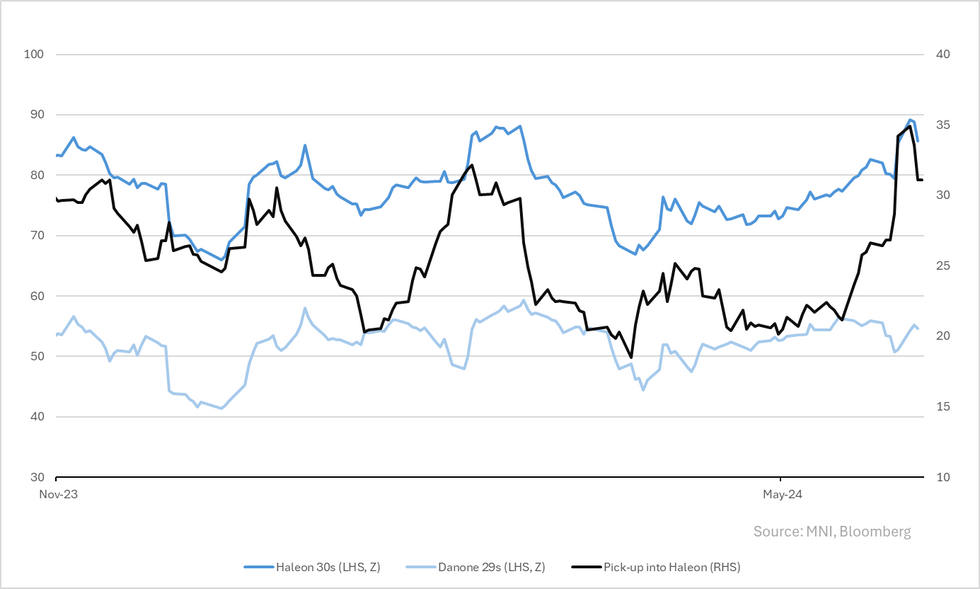

Sector cheap views on Haleon 30s (Z+86) and new Barry Callebaut 29s (Z+106)

- Danone, the parent of dairy, water & nutrition brands including Activia & Alpro, is giving guidance for +3-5% LFL net sales growth between 2025-28 and EBIT margin growth. This is identical to it's FY24 guidance. Analyst consensus is there on both.

- It's also targeting double digit ROIC & "progress towards its LT ambition of €3b FCF" (from €2.6b in FY23).

- Nothing on BS. It ended FY23 net 2.8x & gross 5.3x levered on €3.65b of EBITDA. As we said when it came to issue in late April we don't expect rating changes. Leverage did spike tad higher in FY23 (from net 2.5x last year) but that was on weaker headline which it seems to now be turning around (last 2 quarter saw volume growth). FCF generation gives it a lever to control debt down as needed; FCF/net debt at 25%, to gross at 17%.

- Cheap bonds in the sub-sector are on the Haleon30s that gives +25bps in spread pickup over the curve (against the Danone 29s below).

- We think investors have given Haleon the cold shoulder after GSK and Pfizer linked heartburn drug Zantac and its linked cancer lawsuits. Haleon has and continues to distance itself from any liability/link noting it spun-off from GSK in 2022. Full response from Haleon here.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok