Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

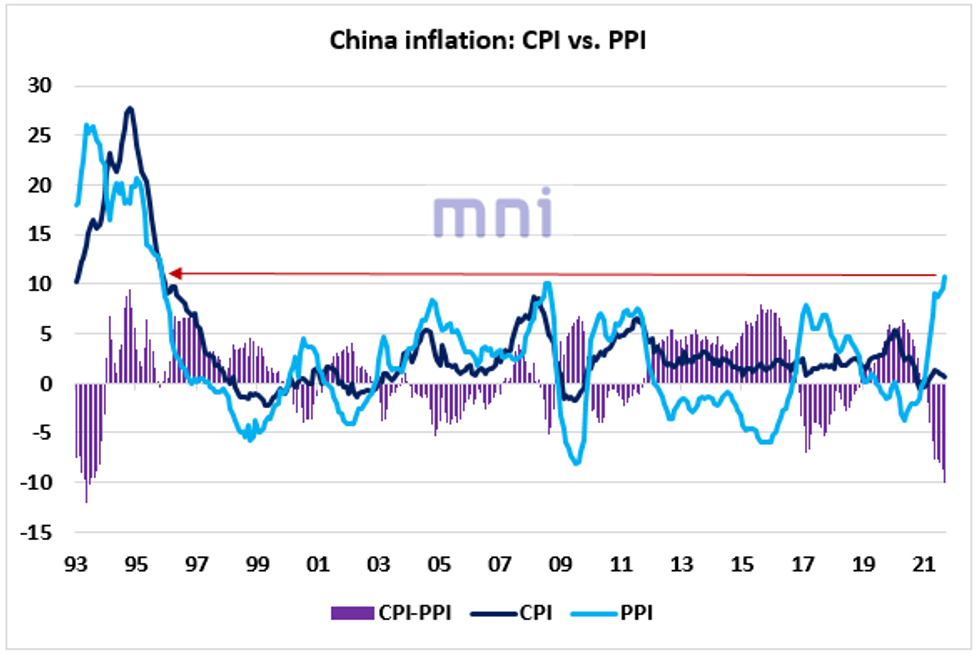

- We saw overnight that while CPI inflation in China continues to decelerate (+0.7% YoY in September), PPI surprised positively (again) surging by 10.7% YoY, the highest since November 1995 (chart below).

- It is interesting to see that the relationship between the two times series, which was quite strong before the 2008 Financial Crisis, broke down in the past cycle.

- China LT bond yields have been more sensitive to PPI inflation (rather than CPI inflation) in the past 10 years (to the exception of 2021: bond yields have remained low in 2021 despite rising inflationary pressures).

- Hence, we have been attributing more importance to Chinese PPI when computing our liquidity and real money growth indexes.

- We recently saw that major indicators are showing two different outlooks for China PPI inflation:

- On one hand, the sharp contraction in China credit impulse is pricing in a disinflationary outlook in the coming 6 to 12 months;

- On the other hand, the rise in energy commodities with coal futures rising to record levels could continue to send China inflation to new highs in the near term.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok