Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

NORGES BANK

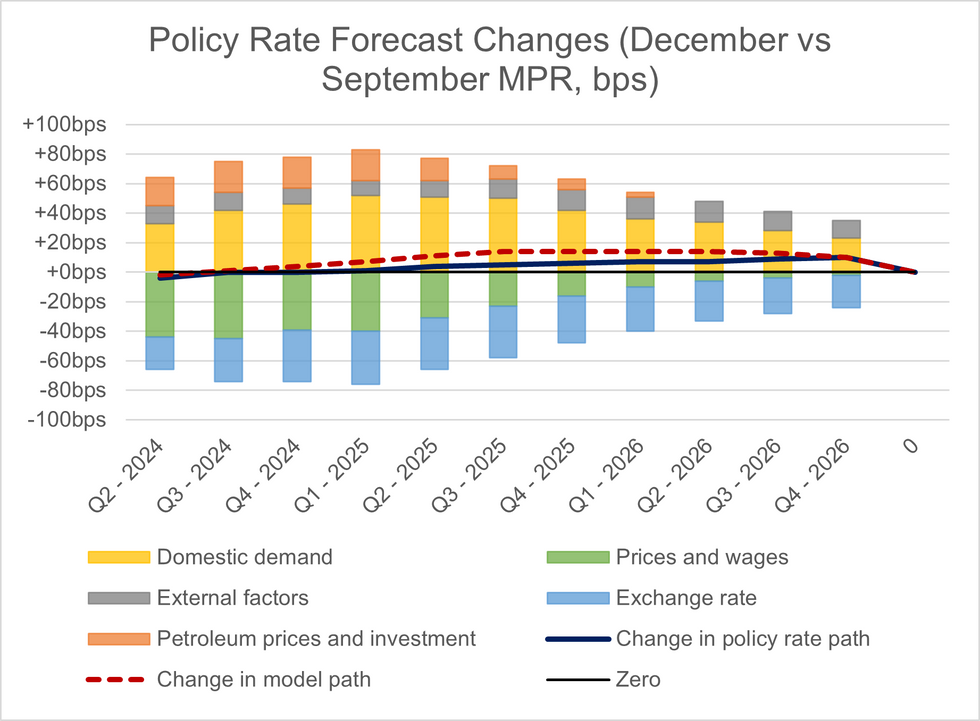

The Norges Bank's revised policy path was little changed through the forecast horizon. Most analysts, including MNI, expected a larger downward revision due to recent developments in inflation and the NOK.

- The first full 25bps cut is still seen in Q4 2024, in line with the repeated guidance that the policy rate needs to be held at current levels for "some time ahead".

- Perhaps even more surprisingly, the "judgement factor" (i.e. the difference between the model implied path and the actual policy path) was negative through the policy horizon. This means the Norges Bank revised the actual policy path below what their model predicted.

- A first glance at the data shows that the contributions of each component of the policy path were in line with expectations (e.g. prices and wages and the NOK contributed negatively).

- However, the upward contribution of domestic demand and petroleum prices and investment appears much larger than analysts were looking for.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok