Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

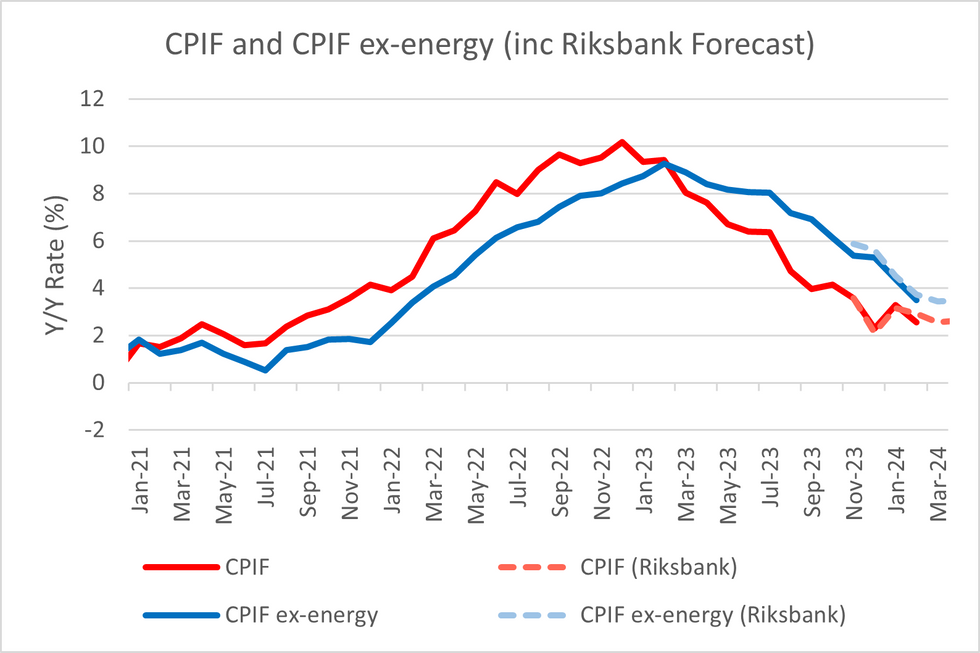

Swedish February CPI surprised to the downside on the headline and core CPIF measures. EURSEK saw a ~0.15% knee-jerk higher on release but was unable to breach the 20-day EMA at 11.2155, now up less than 0.1% on the day.

- CPIF ex-energy was 3.5% Y/Y (vs 3.6% cons, 4.4% prior). Headline CPIF was 2.5% Y/Y (vs 2.8% cons, 2.9% Riksbank and 3.3% prior)

- The Riksbank's November MPR projection CPIF ex-energy was for 3.7% Y/Y. Combined with the other data we have received since the February monetary policy meeting (e.g. survey evidence on pricing plans), today's data supports a cut in the first half of 2024.

- Food and alcoholic beverages were expected to decelerate due to base effects, but the 0.1% M/M rise was softer than the 0.5 to 0.6% M/M estimates we had seen from some analysts. The annual rate was 1.2% Y/Y (vs 3.8% prior).

- Core goods components also moderated in February, with furniture and household goods inflation at 1.2% Y/Y (vs 3.1% prior).

- Services components were more mixed, but moderations in restuarants and hotels (4.2% Y/Y vs 4.9% prior) and recreation and culture (3.3% Y/Y vs 4.5% prior) should help the overall services category decelerate on the year.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok