Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

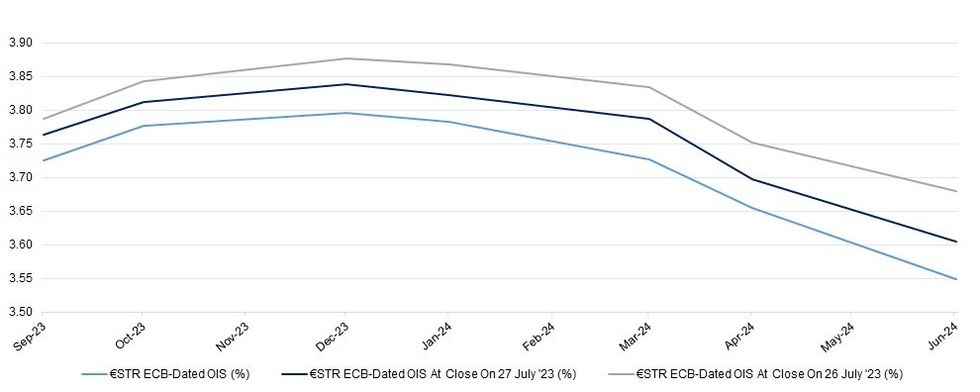

The liquid area of the ECB-dated OIS strip runs 4-6bp softer today as Villeroy underscored the data-dependent nature of the Bank’s future policy choices, while pointing to growing confidence in a disinflationary path.

- Elsewhere, some of the usually hawkish leaning Governing Council members provided less forceful tones surrounding the need for further tightening, while Stournaras remained on the dovish side of the spectrum.

- It wasn’t all dovish though, with Kazimir and Nagel sticking to the hawkish side of the divide, albeit seemingly open to a pause in September, if the data warrants it.

- As President Lagarde noted yesterday, the burden of proof will lie with the data and that leaves the optics of the ECB rhetoric looking more dovish than just a few short weeks ago.

- German HICP data will have provided some background support for the prevailing dynamic, at the margin.

- Pricing is through yesterday’s dovish extremes, with only ~7bp of tightening showing for September and terminal deposit rate pricing hovering around 3.90% (assuming the latest 25bp rate hike is fully passed through into the ESTR space).

- A 25bp cut from current terminal rate pricing levels is now essentially fully priced in for June ’24.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Hike-Adjusted Effective €STR Rate (bp) |

| Sep-23 | 3.7251 | +7.2 |

| Oct-23 | 3.7771 | +12.4 |

| Dec-23 | 3.796 | +14.3 |

| Jan-24 | 3.7828 | +13.0 |

| Mar-24 | 3.7266 | +7.4 |

| Apr-24 | 3.654 | +0.1 |

| Jun-24 | 3.549 | -10.4 |

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok