Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

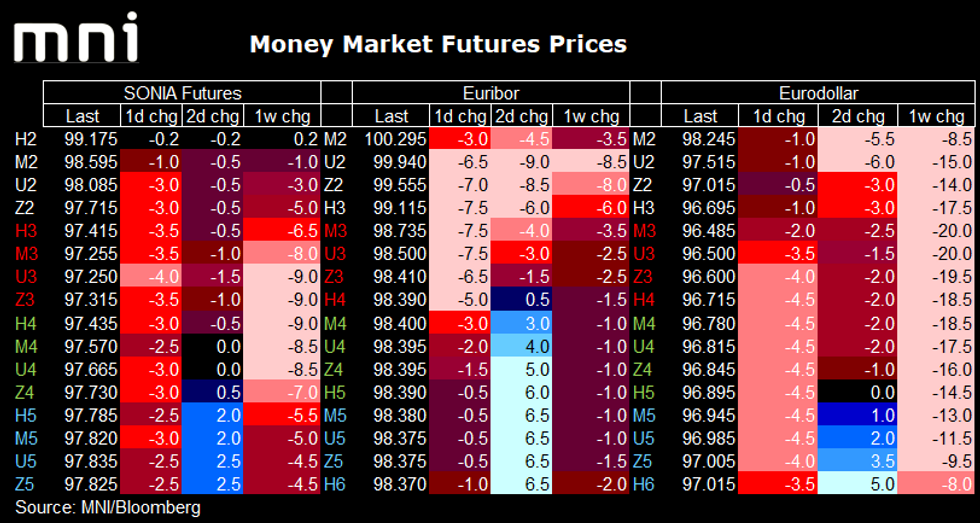

STIR FUTURES

- STIR futures are lower across the board this morning, led by a move lower in the Euribor strip. This has been triggered by some hawkish comments from ECB Governing Council members. First, Belgian National Bank Governor Wunsch stating that July is in play for a first rate hike and that rates could move into positive territory this year. Second, comments from de Guindos (seen as more influential as he is on the ECB's Executive Board rather than a national governor). He also said that rates could rise as soon as July or September. He outlined the future path of rates less explicitly, but it was still enough to push the Euibor strip lower.

- Euribor Whites / Reds are down up to 7.5 icks on the day wit hGreens 0.5-3.0 ticks lower. Blues are just 0.5-1.0 tick lower on the day. Markets still price less than 2bp for June but now priced almost 20bp for the July meeting, over 5bp higher than yesterday's close and around 7bp higher than Tuesday. A cumulative 41bp is priced for September, 54bp for October and 70bp by year-end (earlier this morning this spiked to over 75bp on the de Guindos comments).

- SONIA futures ar egenerally down 2.5-4.0 ticks across the curve while the Eurodollar curve has steepened through the Reds with some Reds / Greens / Blues up to 4.5 ticks lower on the day.

- The 150bp priced in for the UK for the remainder of 2022 is little changed (an average of one 25bp per meeting). There are 2-3bp more priced in for the Fed this morning with just over 225bp priced for the remaining 6 meetings (three 50bp hikes and three 25bp hikes).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok