Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ASIA

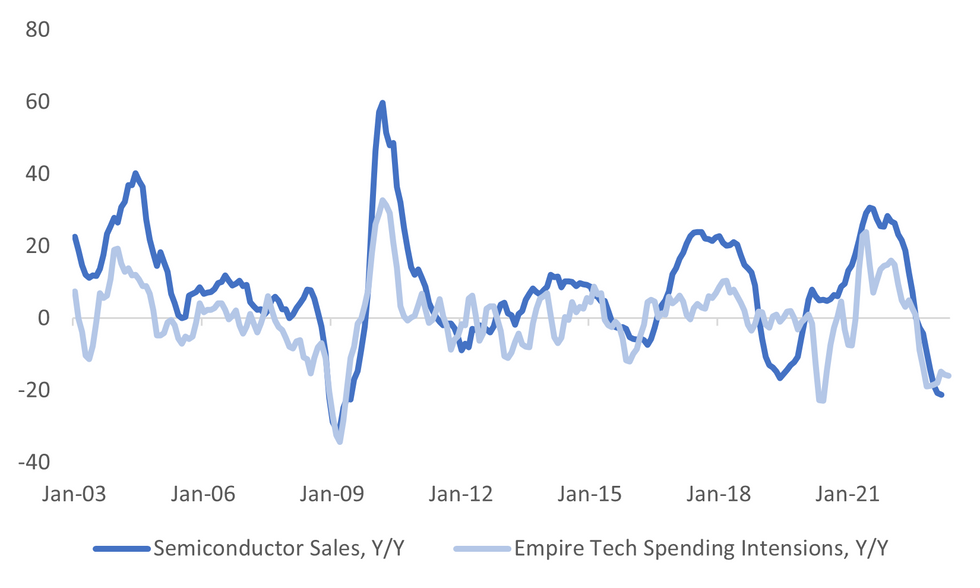

The US Empire manufacturing reading for May slumped, printing at -31.8, versus -3.9 expected (prior was 10.8). The market impact following the release wasn't large, as it tends to be quite a volatile series, particularly relative to other business surveys. Still, we did see fresh lows back to the first half of 2020 in terms of the sub-component related to 6 month ahead technology spending intentions (+1.9 from +10.3).

- The chart below plots the y/y change in such intentions (smoothed as a 3 month moving average) against y/y global semiconductor sales.

- Waning tech spending intentions suggests fairly limited prospects for a sharp turnaround in global semi conductor sales, in the near term at least. Up to March, sales to the US were -16.43% y/y, to China -34.05%, rest of Asia Pac -22.2% y/y, while sales to the EU and Japan also slipped into negative y/y territory.

- Next Monday we also get the first 20-days export data for May in South Korea, which will provide an update on semiconductor exports, which have remained depressed in the first 4 months of this year.

Fig 1: US Empire Tech Spending Intentions Versus Global Semiconductor Sales

Source: MNI - Market News/Bloomberg

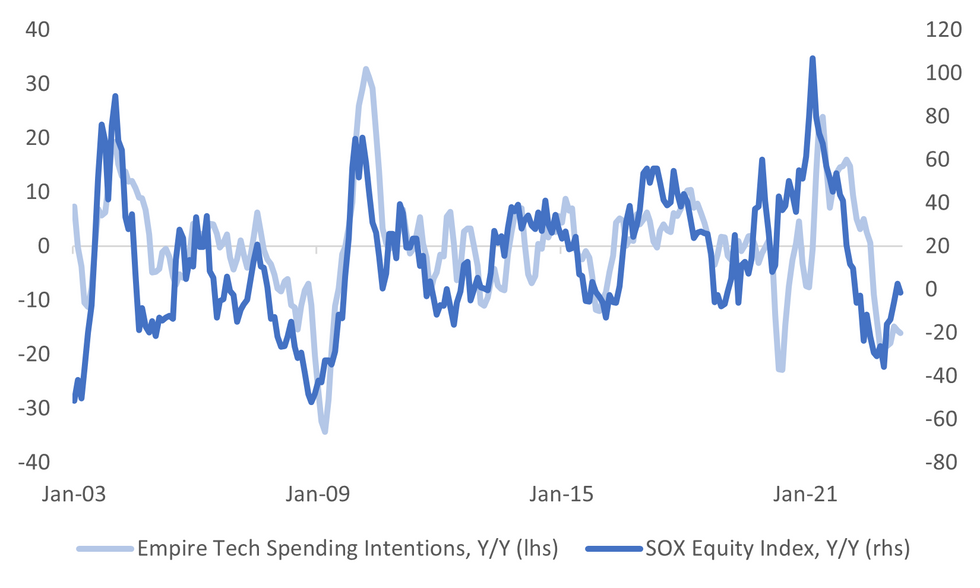

- Still, the SOX semiconductor equity index is painting a slightly less bearish picture. Whilst the equity index is still down in y/y terms, we are well past the trough point from late last year near -36% y/y.

- If the equity index can sustain current levels, we will move back into positive y/y territory for June. This would present a less adverse tech spending backdrop, at least if historical correlations hold.

Fig 2: US Empire Tech Spending Intentions Versus SOX Equity Index

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok