Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

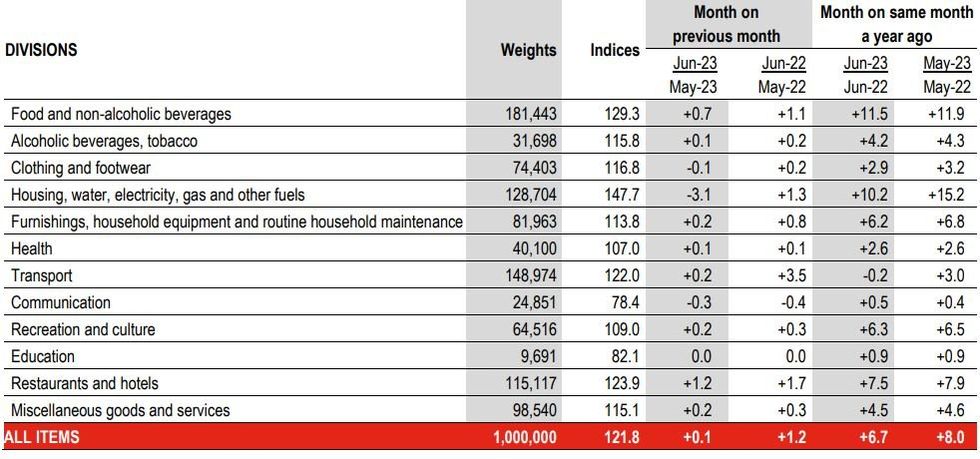

Italy's headline inflation deceleration in June to a 14-month low was faster than expected by the survey median (HICP at 6.7% vs 6.8% consensus, 8.0% prior; CPI 6.4% vs 6.7% expected, 7.6% prior). We would attribute much of the dovish market reaction to relief vs last month's surprisingly strong preliminary print (recall, May flash HICP came in at 8.1% vs 7.5% survey).

- Many analysts had expected an even bigger decline, largely on energy prices (the broad sell-side analyst headline HICP survey range of 6.4-7.2% Y/Y, with CPI from 6.4-6.9%, tells a story in itself of recent Italian inflation volatility).

- And while the report shows progress on core inflation in the 3rd largest eurozone economy (17% of the Eurozone HICP basket), there is a long way to go before it pulls back to comfortable levels.

- Indeed, energy led the way lower for Italian HICP as expected, to a post-Q1 2021 cycle low of 2% Y/Y from 11.5% prior on the back of a sharp fall in non-regulated energy products. More broadly, housing/utility costs slowed sharply (by 5pp to 10.2%).

- With most intrigue on Friday's Eurozone HICP reading surrounding German services prices, at best Italy's report keeps the bloc-wide 5.6% Y/Y headline / 5.5% core flash estimate expectation in play and perhaps nudges consensus lower a couple of tenths of a point.

- That said, June's Italy deceleration was broad-based, and core CPI slowed to 5.6% vs 6.0% in May / core HICP was 6.0% vs 6.4% prior. HICP peaked at 7.0% in February but there hasn't been a print below 2% since prior to the Russian invasion of Ukraine (Jan 2022).

Italy - June Prelim HICP DataSource: Istat

Italy - June Prelim HICP DataSource: Istat

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok