Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

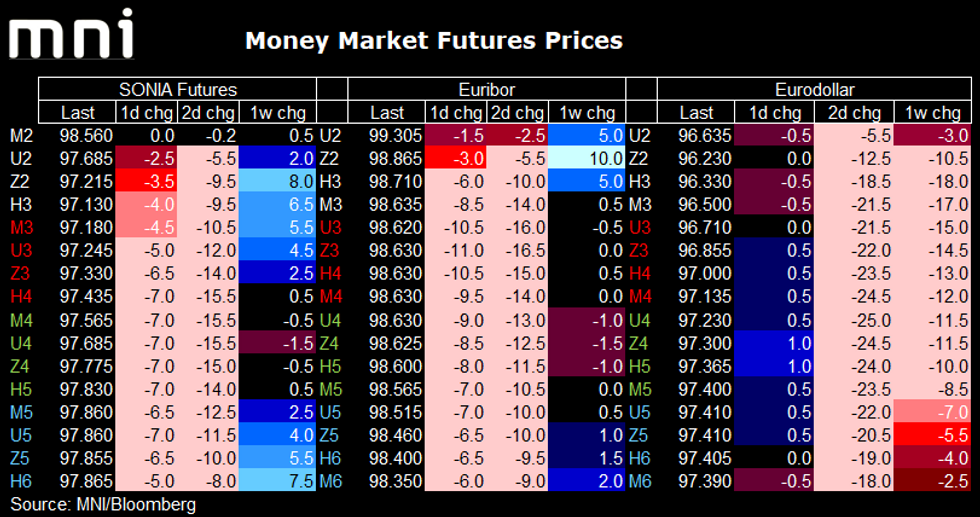

STIR FUTURES

- Euribor and SONIA futures are both lower this morning, with Euribor futures leading the way. The moves started early, possibly helped by the better-than-expected German trade data, and then accelerated following the release of a stronger-than-expected Spanish PMI services print. A weaker Italian services PMI print did not halt the downward moves with upward revisions to French, German and Eurozone prints. Euribor Reds are over 10 ticks lower on the day. Markets now price 44bp for the September ECB meeting, a cumulative 79bp by October and 102bp by the December meeting. No further rate hikes are fully priced.

- The SONIA strip is down up to 7 ticks on the day, dragged lower by Euribor futures in spite of the downward revision to the UK services PMI. Markets continue to price 45bp for tomorrow's meeting (around an 80% probability of a 50bp hike) with a cumulative 90bp priced by September, 129bp by November and 152bp by December. There are also no 2023 hikes fully priced with the curve peaking at 167bp priced in March before inverting.

- Eurodollar futures are all within 1 tick of yesterday's close. Markets price in 61bp for September, 92by by November and 105bp by December. By July 2023 a 25bp cut is fully priced from December's peak pricing.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok