Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

- Core goods prices (-ve factor): Softening producer price data suggests continued weakness in manufactured goods prices, though the shifting around of summer sales periods has made the seasonality of clothing/footwear prices in particular harder to call.

- August EZ non-energy industrial goods 4.7% Y/Y, +0.6% M/M

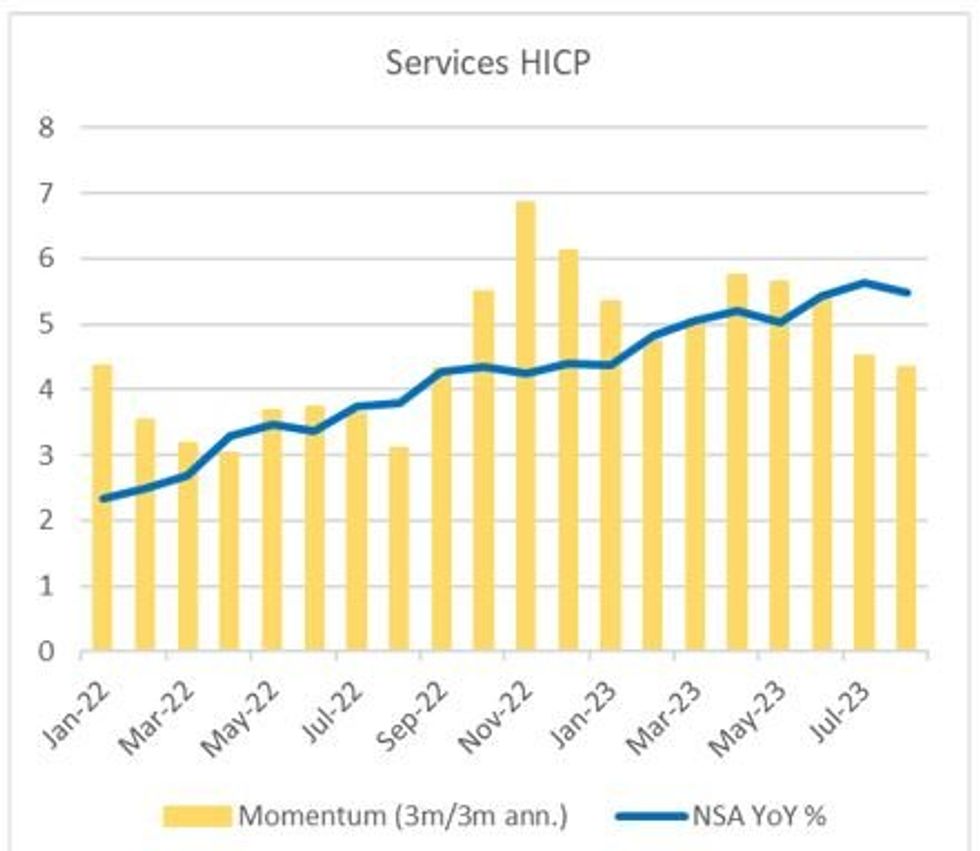

- Overall services prices (-ve factor): Summer 2023 was seen as having represented the peak for services prices, with a variety of volatile categories including airfares and holidays set to moderate in the rest of the year due to both base and weighting effects. Most notably of all, the introduction of the 9 euro transportation ticket in Germany in summer 2022 boosted base effects this year through August but this will drop out in September.

- Some analysts see the September flash PMI data as pointing to stubborn services pressure but not enough to keep this category from weighing down aggregate readings.

- August EZ services 5.5% Y/Y, +0.2% M/M.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok