Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

(MNI Australia) Recent trends were mostly maintained in terms of South Korean first 20-days trade data for March. Export growth was -17.4% y/y, while imports were -5.7% y/y. This is a down step in import growth (the prior read was 9.3% y/y for the first 20-days of Feb), but the trade deficit persisted at $6.323bn.

- Looking at the detail showed average daily exports were -23.1% y/y, so still quite depressed as well. Chip exports remain a weak point, -44.7% y/y. This is consistent with what officials have said in terms of external headwinds persisting in the first half. They are more optimistic around better export trends in the second half of the year.

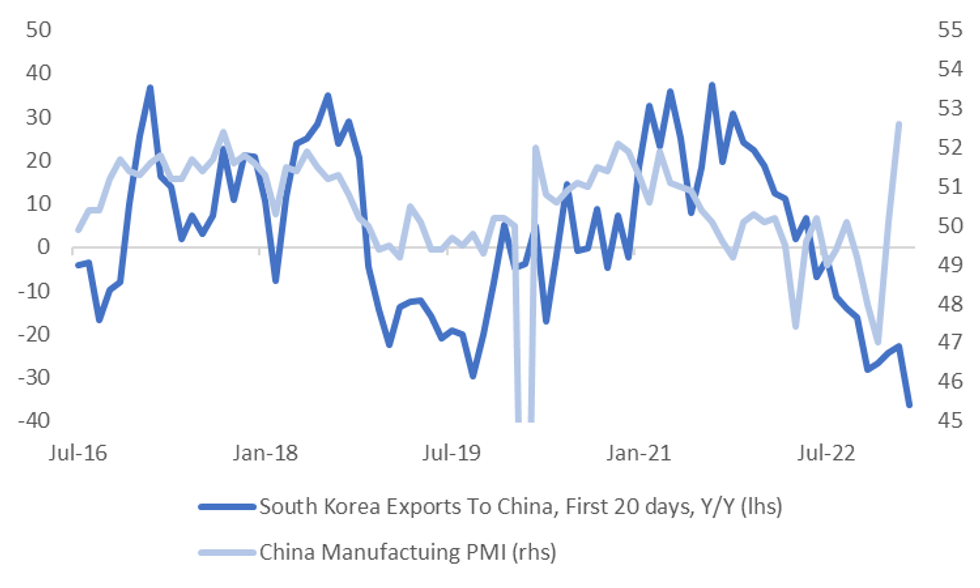

- By country, China exports remained depressed, down -36.2% y/y. As we progress further into 2023 base effects should support some recovery. Still, this weakness is at odds with recent indicators like the China manufacturing PMI, see the chart below.

- One possibility is the PMI is overstating the strength of the recovery in China. Activity indicators for Jan-Feb didn't paint as upbeat picture as implied by the PMI. Trade tensions with the US, particularly in the tech space, may also be leading China buyers to shy away from South Korea, given broader strategic alliances.

- It could also be the case the China recovery will show up in firmer exports from South Korea with a lag.

- Note exports to US, for the first 20-days of March, remained resilient at +4.6% y/y.

Fig 1: South Korean Exports To China Still Struggling

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok