Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

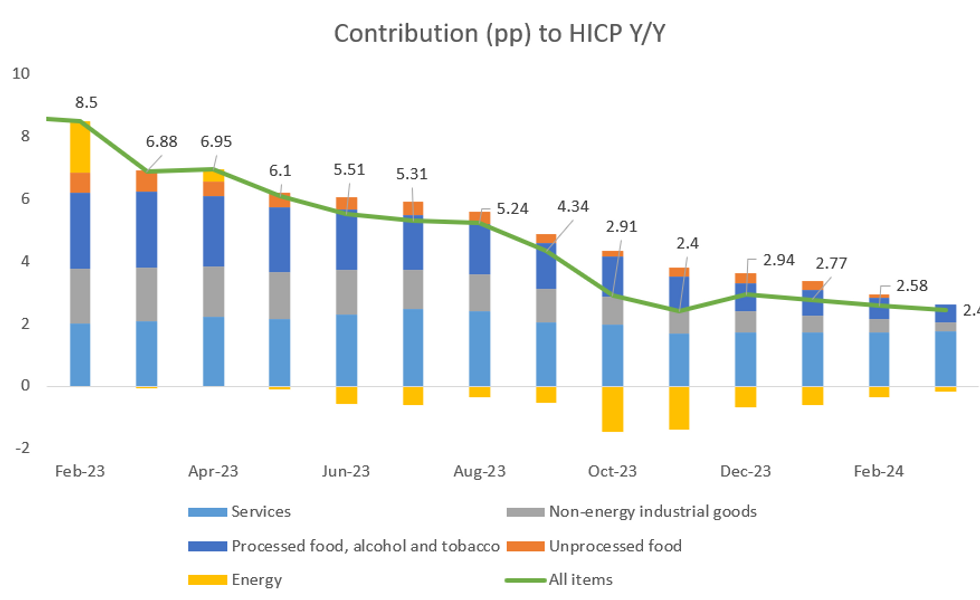

Eurozone Final HICP confirmed the March flash print. Energy and Unprocessed food both saw Y/Y disinflation between February and March, whilst Processed food, alcohol & tobacco and NEIG continued to see Y/Y disinflation. The March prints were confirmed at +2.4% Y/Y (vs +2.6% Y/Y in February) and +0.8% M/M (vs +0.6% M/M in February).

- Similarly, core inflation on an annual basis printed in line with flash at +2.9% Y/Y (vs +3.1% Y/Y in February), although on a monthly basis it saw a rise to +1.1% M/M from +0.7% M/M in February.

- At a country level: Slovakia saw a revision from flash HICP Y/Y up +0.2ppt, Spain and Lithuania saw a +0.1ppt revision to flash Y/Y HICP whilst Italy, Finland and Austria saw HICP revised down by 0.1ppt.

- The final readings show the contribution from services inflation actually rose after two consecutive months of stalling, contributing +1.76ppt, the highest contribution since October 2023 and it remains the largest contributor to the headline inflation rate.

- In contrast, Unprocessed food contributed negatively to headline reading for the first time since the Covid pandemic, printing at -0.02ppt (vs +0.1ppt prior).

- Meanwhile, Processed food, alcohol and tobacco contribution fell to +0.55 ppt (vs +0.69ppt prior) - the lowest contribution since January 2022. In addition, NEIG's contribution fell again to +0.30ppt (vs +0.42ppt) - remaining the lowest contribution since July 2021.

- Energy's negative contribution continues to fade as highlighted in our inflation insight as base effects continue to drop out of the Y/Y comparison, recording a contribution of -0.16 ppt in March (vs -0.36ppt in February).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok