Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

A few thoughts on the unfolding SVB Financial situation and what it means for Fed policy:

- SVB's story and share price collapse yesterday appears to be fairly straightforward: rising US interest rates resulted in a combination of 1) losses on MBS and other fixed income security holdings 2) increasing short-end funding costs (ie rates paid on client deposits) 3) SVB's unusually high exposure to the waning tech/start-up space (which meant deposit flow has dwindled vs huge inflows in 2019-21 during the tech boom).

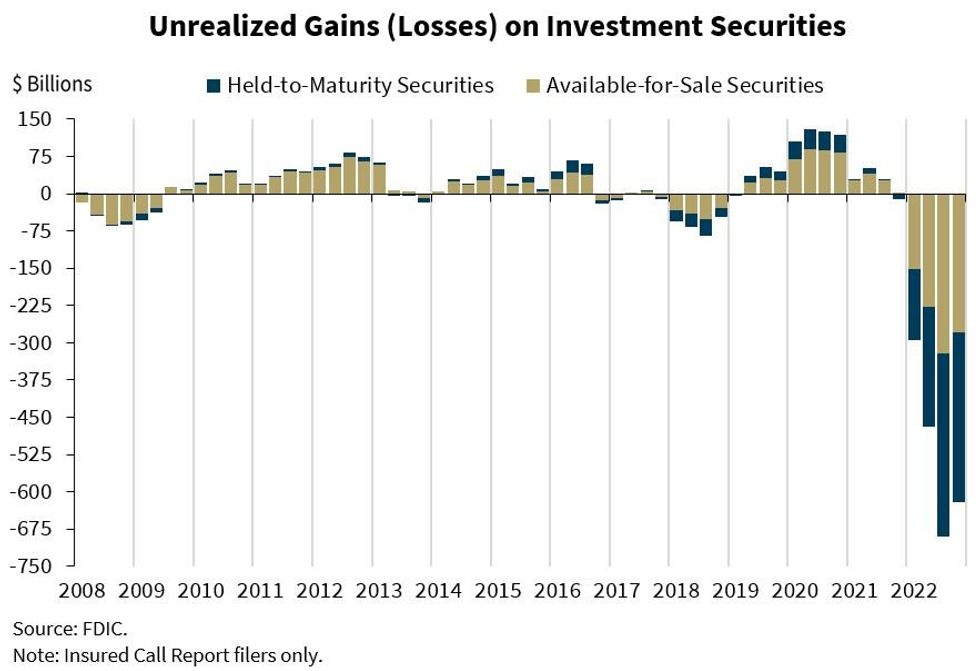

- The first issue of unrealized losses on fixed income securities as rates rise is well known across the sector - take for example the chart below from the FDIC's Q4 banking profile showing a total $620B of unrealized losses as of Q4 2022. SVB yesterday decided to realize their paper losses and raise equity, which came as a surprise. With large unrealized losses remaining, and their decision yesterday to realize some now, there remain questions over whether they will have to sell more to cover a loss of client deposits which may leave the bank amid this crisis (as widely reported overnight).

- The second appears to be an increasing problem for deposit-dependent banks, which are having to compete for funding with the likes of risk-free 6M Tbills paying 5+%.

- From a systemic perspective, this all appears to be manageable. With regulation since then, it is not like 2007-08 when banks were under-capitalized and had massive amounts of high-risk assets on the balance sheet. But clearly, the rapid Fed rate hike cycle of the past year is beginning to create cracks in the banking system.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok