Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

MNI (London)

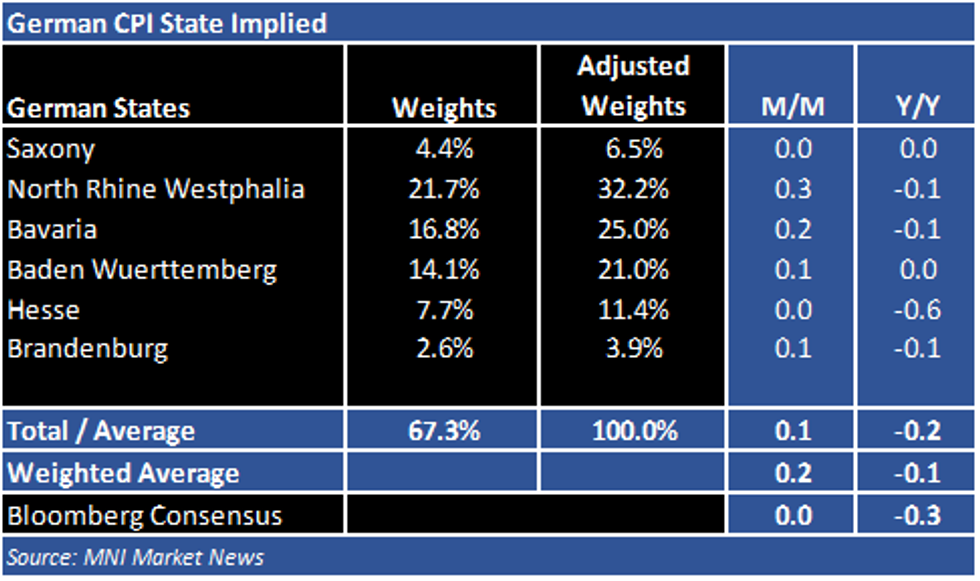

CPI: Bbg: 0.0% m/m, -0.3% y/y; Prev (Sep): -0.2% m/m, -0.2% y/y

HICP: Bbg: 0.0% m/m, -0.4% y/y; Prev (Sep): -0.4% m/m, -0.4% y/y

- MNI's analysis of state-level CPI data from the six states that have published so far (just above 67% of national total) suggests pan-German inflation will come in stronger than market expectations.

- Our estimate points to a CPI drop of 0.1% on an annual basis, while the monthly rate is seen flat in Oct

- The y/y HICP dropped to -0.4% in Sep, marking the second negative reading this year and and the lowest level since Jan 2015.

- Sep's downtick was mainly driven by the German VAT cut, which was implemented in July and has had a negative effect ever since.

- Energy prices showed another y/y decline in Sep and Destatis noted that prices would have risen 0.6% excluding energy prices

- Food inflation continued to increase modestly in Sep.

- Survey evidence also suggests a upside risk as well:

- The recently released flash composite PMI noted that prices charged for goods and services rose for the first time since Feb, reflecting increases in the service and mfg sector.

MNI London Bureau | +44 203-865-3814 | irene.prihoda@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok