Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

A key theme in recent Fed communication over the past couple of weeks has been the importance of inflation expectations. Namely, that FOMC members are unconcerned with near-term inflation pressures (as seen in the April CPI report) as longer-term market-based metrics suggest that inflation expectations remain well-anchored.

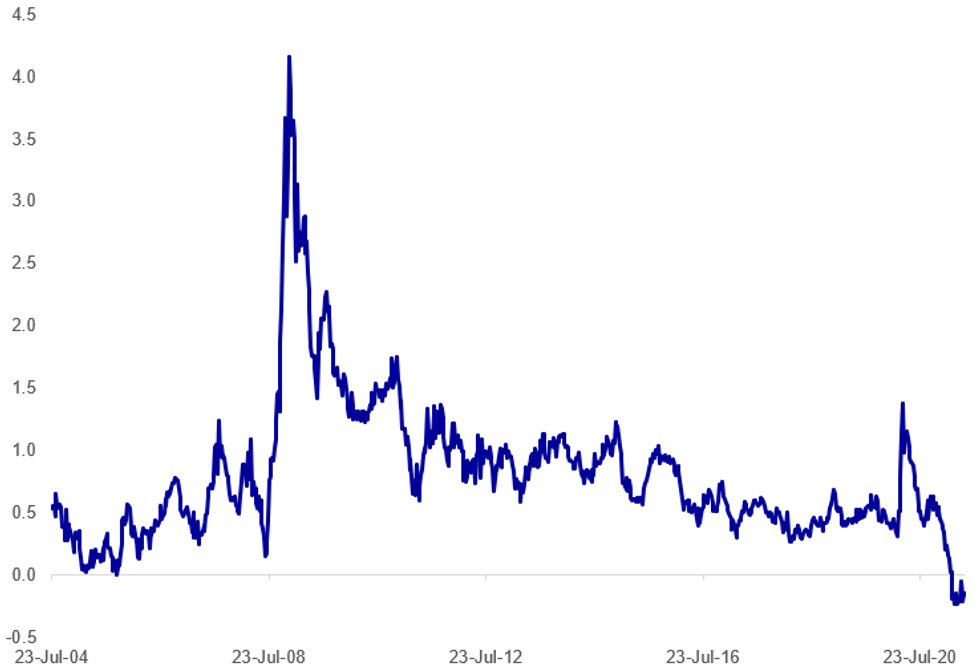

- Specifically, Vice Chair Clarida last week, and St Louis Fed Pres Bullard (in an MNI interview) this week pointed to 5Y5Y inflation forwards trading below 5-Yr TIPS implied breakevens as a sign that a rise and potential 'overshoot' of the Fed's 2.0% average target is possible over the coming 5 years, but it's not expected to spiral over the subsequent 5 years (see chart below).

- It would usually be the case that 5Y5Ys would be trading higher vs 5Y B/Es. But the spread's been trading below 0% sustainably since February, the first time in the series history (back to 2004).

- Bullard's other criteria is the level of breakevens, as he told MNI the 5Y B/E would have to be "considerably higher than it is today", pointing to >2.75% B/Es (equating to 2.45% PCE prices, which is his desired degree of overshoot). 5Y TIPS breakevens are last trading 2.63%, with 5Y5Y Fwds at 2.49%. So there is room to go yet on both the spread and the breakeven before Bullard's criteria for what he called getting "more active in trying to reassure markets" about inflation anchoring.

US 5Y5Y Inflation Swap Minus 5Y TIPS Implied BreakevenSource: BBG, MNI

US 5Y5Y Inflation Swap Minus 5Y TIPS Implied BreakevenSource: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok