Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JGBS

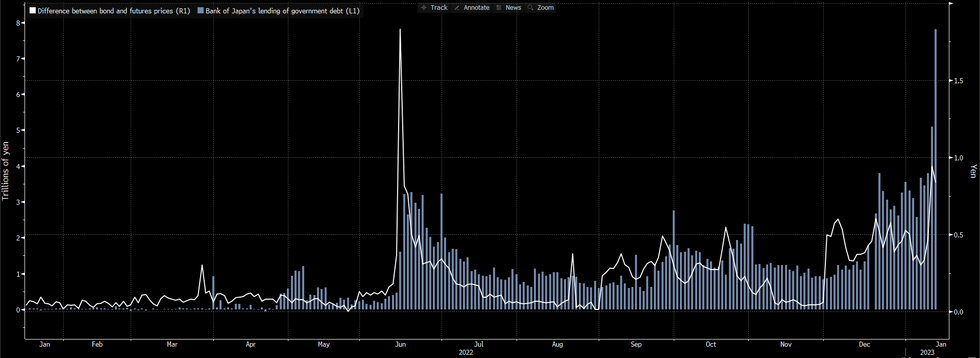

BBG’s measure of basis between the pricing of JGB futures and their underlying bonds has moderated from the pre-BoJ spike higher (which didn’t get anywhere near challenging levels witnessed back in the mid-’22 attack on the BoJ’s YCC parameters).

- The BoJ’s choice to leave its monetary policy settings unchanged, coupled with the well-documented tweaks to the parameters underlying the Bank’s Funds-Supplying Operations against Pooled Collateral (a further backstop to its YCC settings), and the subsequent demand for JGBs related to and coming via that facility (whereby cheap borrowing finances received positions in swaps and longs in JGBs), resulted in a ~360 tick trough to peak rally for futures in recent sessions.

- Still, the basis measure identified remains elevated in a historical sense as the BoJ continues to face market functioning issues that are a product of its upsized JGB purchases against already large JGB holdings (short cover in certain illiquid cash bonds may be keeping a floor on the basis even after futures pulsed back from their YCC speculation induced lows, while other bonds may not even be trading), while continued positioning for a future tweak to BoJ policy settings via futures (albeit less extreme than pre-BoJ levels) also works in the same direction when it comes to basis.

- This is a huge issue when it comes to market efficiencies and makes the JGB futures contract a far less effective hedge for positions in underlying cash JGBs.

Fig. 1: BBG JGB Futures Net Basis Measure Vs. BoJ Lending Of JGBs

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok