Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ASIA

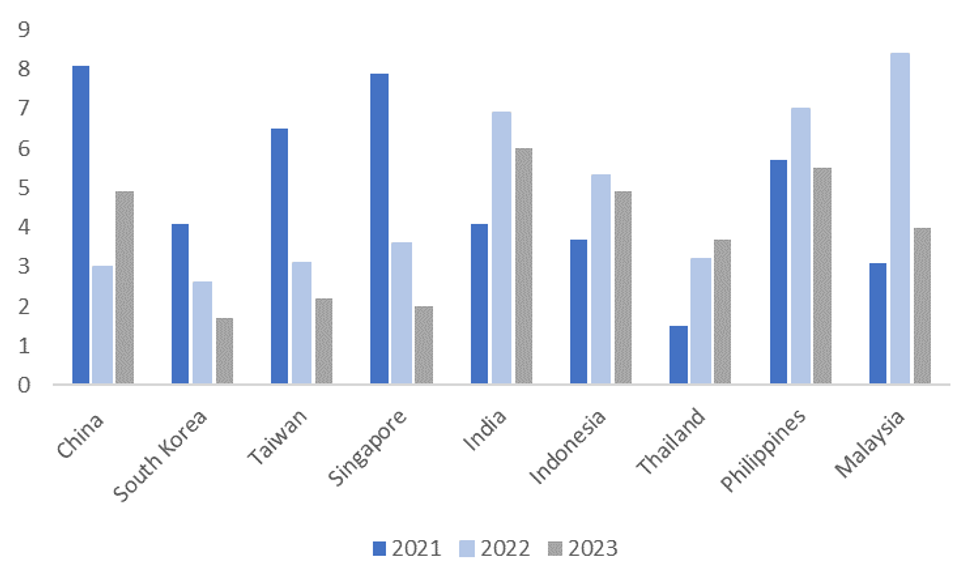

Consensus expectations, taken from Bloomberg, for EM Asia GDP growth next year are mostly down on projected 2022 outcomes, see the first chart below.

- The export orientated economies are expected to see decent falls, -0.9 to -1.6ppts across South Korea, Taiwan and Singapore. Malaysia sees the largest absolute fall of -4.4ppts, but outright growth is still expected to healthy at +4% for next year.

- South Korea has the lowest absolute growth forecast of 1.7%, with weaker export growth and tighter domestic financial conditions headwinds.

- The more domestically orientated economies in terms India, Indonesia and the Philippines are also expected to see lower growth, albeit still at elevated rates relative to major developed economies.

- China and Thailand are the clear exceptions where the market is forecasting improved growth outcomes in 2023 relative to this year. For China this largely reflects the shift away from CZS, while Thailand is also expected to benefit from a further recovery in tourism inflows.

Fig 1: EM Asia Growth Forecasts, Slower 2023 Expected (ex China/Thailand)

Source: MNI - Market News/Bloomberg

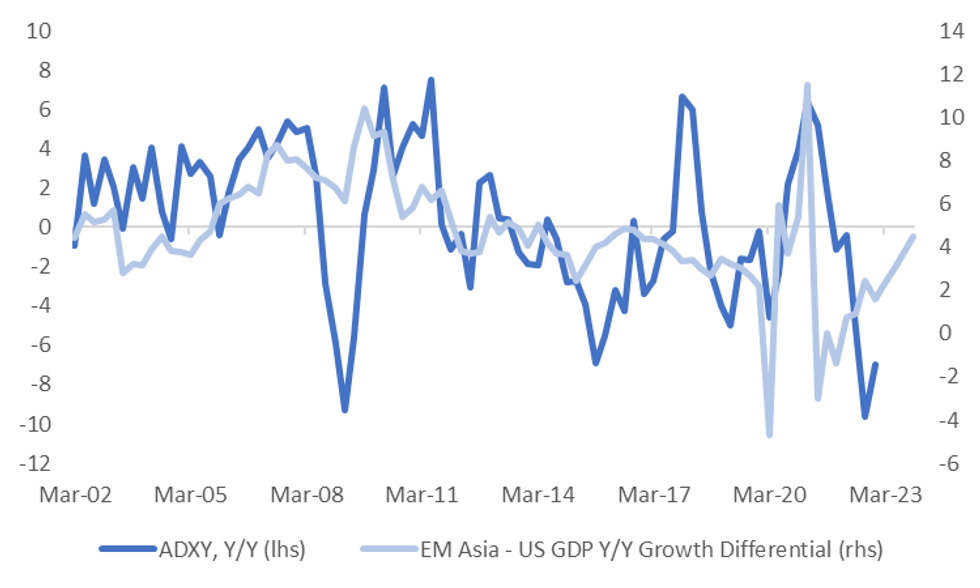

- Despite these downside expectations for most EM Asia economies, the projected growth differential with the US is still forecast to either stay flat in 2023 relative to 2022 or improve for all economies in the region (except Malaysia). The same also applies against the EU area.

- The second chart below plots the y/y change in the J.P. Morgan Asian currency index against the regional growth differential with the US (we project this differential into 2023 using the above consensus forecasts).

- This picture suggests a less adverse backdrop for broader Asian currencies into 2023 compared to this year, assuming these projections are realized. We also accept there will be other important moving parts for the FX backdrop, like Fed policy and commodity prices/terms of trade outlooks.

Fig 2: EM Asia - US GDP Y/Y Differential Versus ADXY Y/Y

Source: J.P. Morgan/MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok