Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

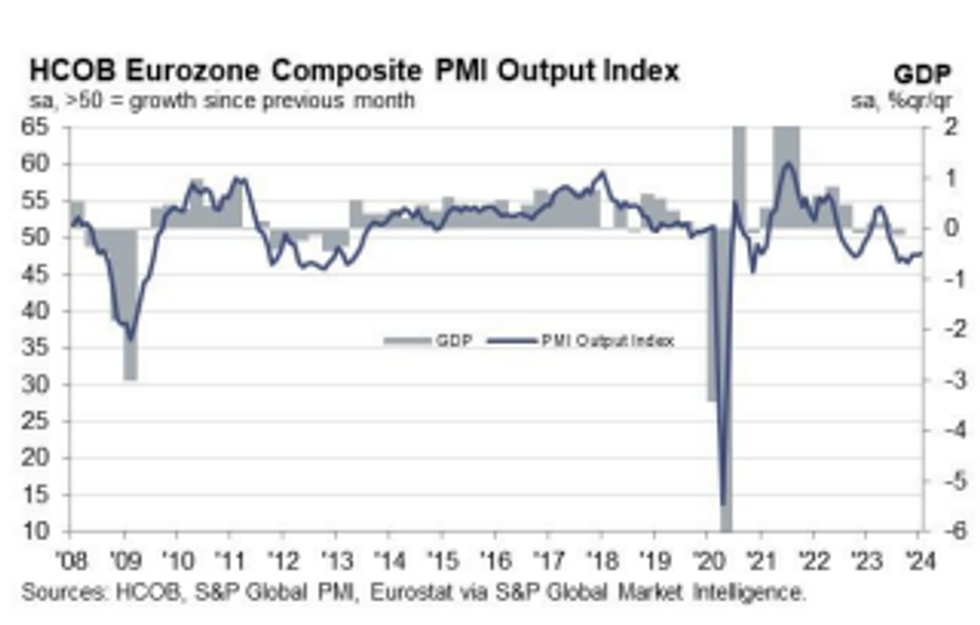

The services component of the Eurozone January flash PMI printed at a below-expected 48.4 (vs 49.0 cons, 48.8 prior), as telegraphed by the French and German misses earlier. The manufacturing component above expected at 46.6 (vs 44.7 cons, 44.4 prior), also partly reflecting the German/French beats, and a 9-month high. The composite reading reached a 6-month high at 47.9 (vs 48.0 cons, 47.6 prior).

Note that the -0.6 point Services miss is smaller than the German (-1.7) and French (-1.0) equivalents, indicating that other EZ countries, namely Italy and Spain, likely performed relatively strongly in January according to the PMI. As the release notes, "the rest of the eurozone [ex- Germany and France] as a whole returned to growth after five months of decline, recording the largest – yet still modest – expansion since last June".

Key notes from the release are:

- "Although disruptions to shipping in the Red Sea caused supply chains to lengthen for the first time in a year, manufacturing input costs continued to fall on average".

- "However, service sector cost growth accelerated during the month, contributing to the steepest overall rise in prices charged for goods and services since last May".

- "Employment increased fractionally in January as a slight upturn in net hiring in the service sector offset an eighth successive monthly fall in manufacturing payroll numbers".

- Falls in manufacturing output and new orders continued to drive the downturn in the EZ, but "the fall in factory production was the smallest witnessed since last April". Meanwhile, "new business placed at service providers fell at the slowest rate since last July, providing a further hint of a cooling in the demand downturn".

- "January also saw the region’s export decline easing, with overall new export orders dropping at the slowest rate for nine months thanks to reduced losses for both goods and services".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok