Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Wednesday’s key data releases complement the numerous economic sentiment releases seen this week. Focus will be on German GfK consumer confidence and the MNI China Liquidity Index, followed by French manufacturing sentiment. Later in the morning markets will be looking for revisions in the final Eurozone inflation print for January.

German GfK Consumer Climate to Improve (0700 GMT)

The GfK German consumer sentiment index is projected to improve again for March, expected to tick up to -6.3 following the January dive to -6.9. Consumer sentiment in Germany is seeing small recoveries in both economic and income expectations, however, increased consumer saving continues to drag on the recovery. Underlying confidence growth stems from easing pandemic restrictions and expectations of easing inflationary pressures.

Yesterday’s German ifo sentiment surprised markets with a strong rebound across economic sentiment, current and future conditions as order books grew with the Omicron-wave nearing its end. This implies that a considerable upside surprise in GfK consumer sentiment is likely, despite Russian-Ukrainian tensions which will likely dampen sentiment in upcoming readings.

China Liquidity Index (0700 GMT)

The MNI China Liquidity Index fell nine points to 33.9 in January, implying a substantial easing in liquidity across China’s interbank money market as the economic conditions index recovered to the highest reading in seven months. Today’s release will provide confirmation of whether liquidity conditions are improving and aiding the economic recovery.

French Manufacturing Sentiment Stable (0745 GMT)

French manufacturing confidence is expected to remain stable at the four-year high of 112, which represents unusually high optimism on the back of improvements in order books and evidence of easing supply bottlenecks.

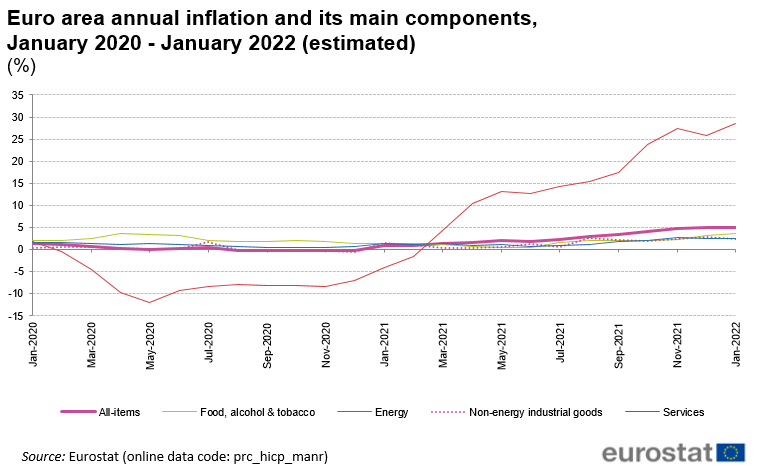

Eurozone Final HICP Print (1000 GMT)

The Eurozone final headline inflation print due this morning is expected to confirm the flash readings and Euro record high of +5.1% y/y and +0.3% m/m in January. The region’s January final releases have seen slight divergence in both Italy and Spain, where Italy’s January final print was 0.2% softer, whilst Spain was 0.1% stronger. This implies that a shift of 0.1% in either direction is on the cards for the Eurozone.

In light of the rising tensions along the Ukrainian border, MNI spoke with a eurosystem source, who highlighted that the ECB would be likely to look through any spike in inflation prompted by higher energy prices as a result of a conflict in Ukraine, and if markets deteriorate would step in to provide liquidity, though there are no signs of significant stress for the moment.

There are multiple key policymaker appearances on today’s schedule, including the ECB’s Frank Elderson and VP Luis de Guindos and the BOE’s Governor Bailey and MPC member Silvana Tenreyro. San Francisco Fed’s Mary Daly is due to hold a keynote speech. Where available, links to events are in the calendar below.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/02/2022 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 23/02/2022 | 0700/1500 | ** |  | CN | MNI China Liquidity Suvey |

| 23/02/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 23/02/2022 | 0915/1015 |  | EU | ECB Elderson Intro & panel participation at Eurofi Seminar | |

| 23/02/2022 | 0930/0930 |  | UK | BOE Governor Bailey et al at TSC | |

| 23/02/2022 | 1000/1100 | *** | | EU | HICP (f) |

| 23/02/2022 | 1130/1230 | | EU | ECB de Guindos Q&A at El Español & Invertia symposium | |

| 23/02/2022 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 23/02/2022 | 1330/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 23/02/2022 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 23/02/2022 | 1500/1500 | | UK | BOE Tenreyro speaks at NIESR Institute lecture | |

| 23/02/2022 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 23/02/2022 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 23/02/2022 | 2030/1530 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.