Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

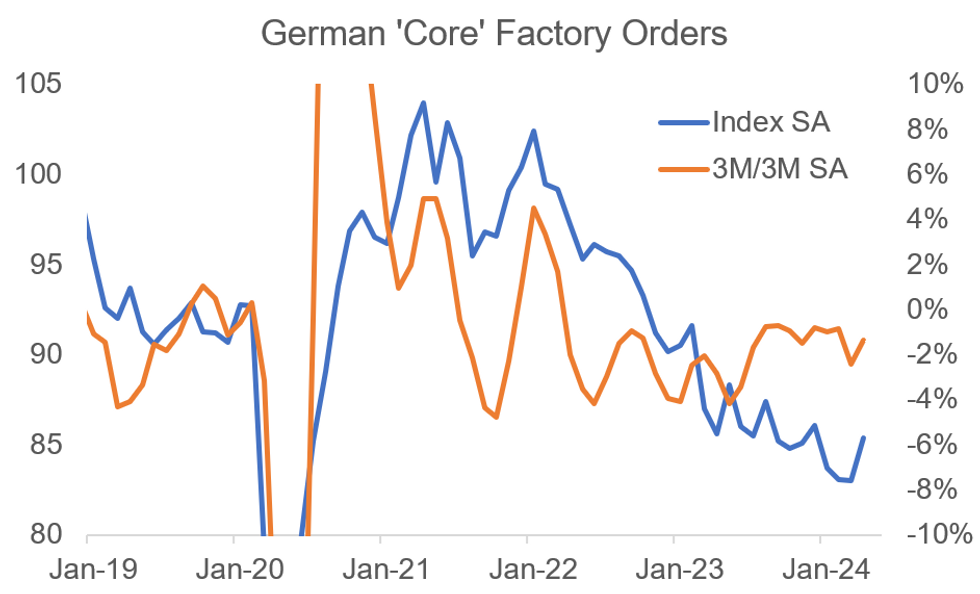

German factory orders declined 0.2% M/M in April, softer than the +0.6% expected and there was also a downward revision to the March print of -0.4pp to -0.8% M/M. The underlying 'core' measure pointed towads some recovery, though.

- Factory orders also declined on a Y/Y basis, by 1.6% (vs +0.3% cons; -2.4% prior, revised from -1.9%), with the renewed improvement in the annual comparison due to base effects.

- Core (ex-large ticket items) orders, a better measure of underlying activity, jumped 2.9% M/M in April (vs -0.1% prior, revised from +0.1%); its less volatile 3M/3M measure also printed stronger than before, at -1.3% in the 3-months to April (-2.4% prior) but this measure remained in negative territory for the 24th consecutive month.

- The breakdown showed the 'core' rise was driven by investment and non-durable goods orders, which came in at +5.2% M/M (vs +0.5% prior; highest rate since the 2020 pandemic recovery) and +4.0% M/M (vs +1.5% prior), respectively. Durable goods orders meanwhile dragged the overall print lower, at -4.3% M/M (vs +3.9% prior).

- Looking at an international split, domestic 'core' orders increased 0.7% M/M (vs -2.2% prior), while foreign orders jumped 4.5% M/M (vs +1.2% prior), driven by EZ orders at +7.4% M/M (vs +2.0% prior).

- Real manufacturing turnover meanwhile decreased 0.9% M/M in April (-0.4% prior, revised from -0.7%), opening up some slight downside risks to the consensus forecast of +0.2% M/M re April's factory orders data.

- Overall, the data adds to the view that there seems to be a gradual recovery of German economic activity forming - but that this recovery is, to a significant extent, externally-driven.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok