Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BELGIUM

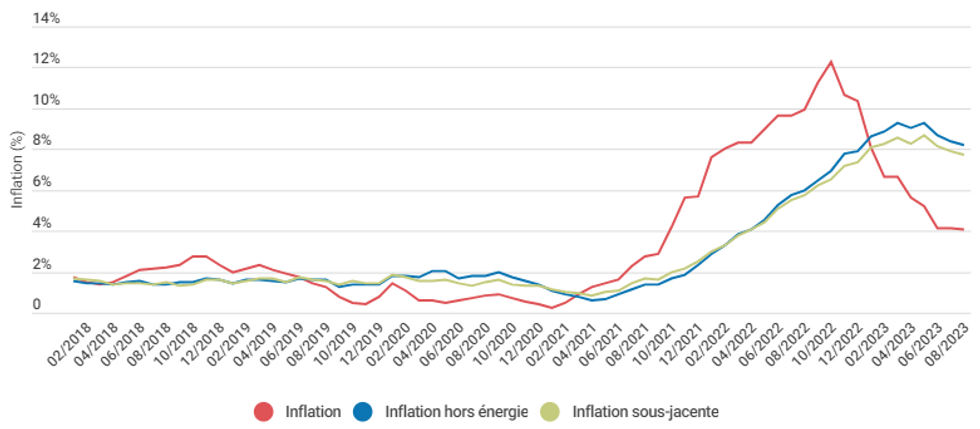

Belgian CPI came in at 4.09% Y/Y / 0.76% M/M in the August flash estimate, vs 4.14% Y/Y / 0.81% M/M prior. Owing to methodological differences, the HICP reading was much lower than this, coming in at 2.4% Y/Y - but a large acceleration vs 1.7% in July and 1.6% in June.

- There is no consensus figure for Belgian CPI or HICP - the country has a 4% weighting in the Euro-wide basket.

- Core inflation metrics fell for the 3rd consecutive month, with ex-energy/unprocessed food at 7.70% in August vs 7.88% in July and 8.14% in June, and 8.70% at the cycle peak in May.

- Per StatBel, fuels, hotel rooms, confectionery, breads and cereals, alcoholic drinks, non-alcoholic drinks, organized holidays in Belgium and personal care represented upside pressures, while electricity, fruit, and plane tickets had a downward effect.

- There was continued large Y/Y deflation in energy, coming in at -22.83% Y/Y vs -24.11% prior (dragging on headline inflation by 3.07pp), as electricity prices fell -36.2% vs 27.1% prior and natural gas -65.2% vs -62.4% prior.

- However this was offset by a jump in heating oil prices (+35.6%) as a gov't subsidy dropped out of the base. Natgas prices were +3.9% M/M while electricity prices were -2.5%, with the stats agency citing changes in tariffs and excise duties.

- Food prices (12.73% vs 13.23% prior) and rent (6.07% vs 6.14% prior) disinflated, but services inflation remained stable at 7.26% vs 7.25%. The health index decelerated from 4.80% to 4.16%.

Source: StatBel

Source: StatBel

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok