Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

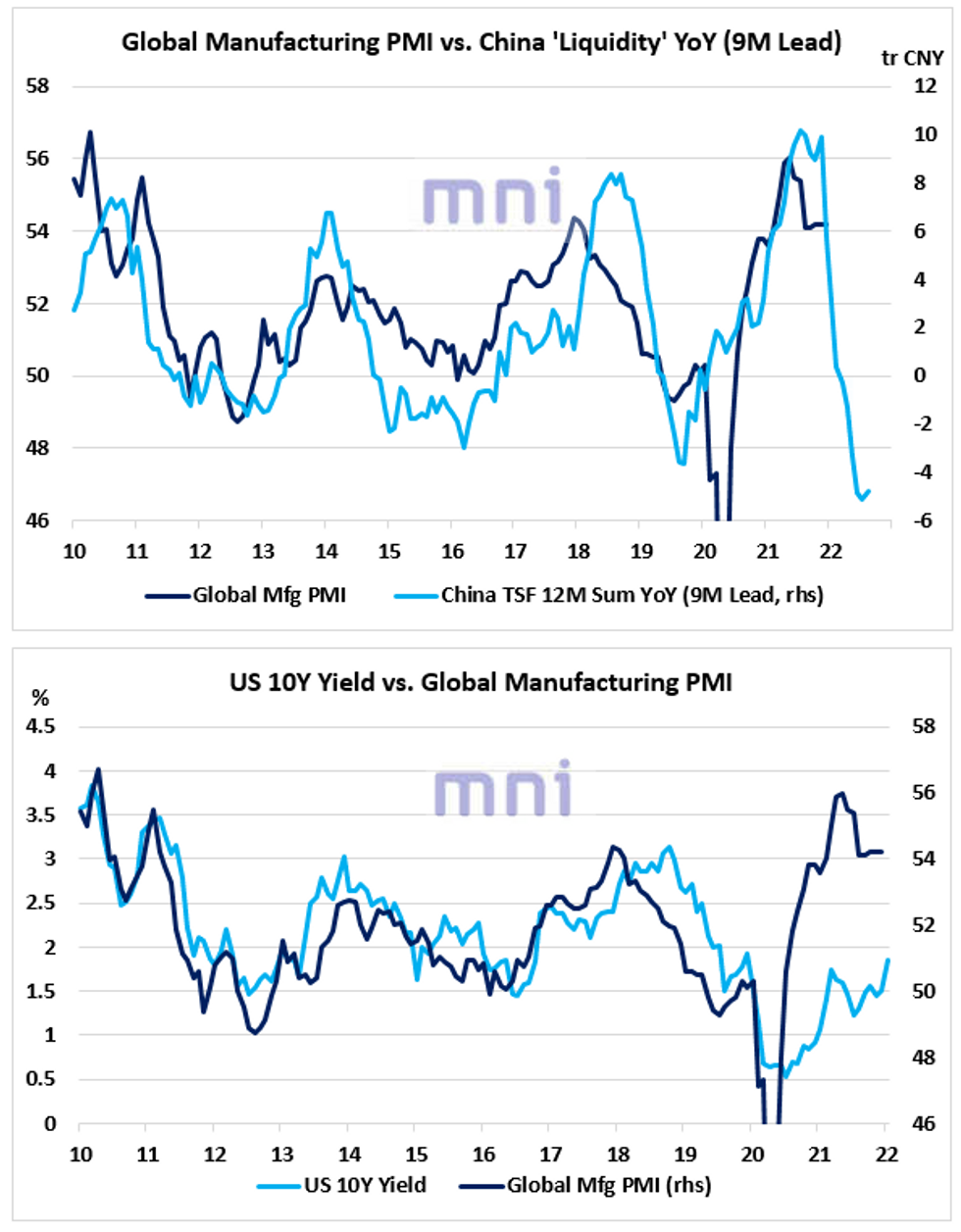

- Even though China has entered an easing cycle through rate cuts (RRR, LPR) combined potentially with an increase in liquidity, the sharp ‘2021 tightening’ could continue to weigh on the global economy and international asset prices.

- Last year, the annual change in the Total Social Financing 12M Sum (our liquidity measure) fell from a high a 10tr CNY to nearly -5CNY , which has increased investors’ concerns over the economic outlook as China ‘liquidity’ has acted as a strong leading indicator of risk aversion.

- The top chart shows how strongly the annual change in China liquidity has led the gauge of global economic activity in the past cycle, measured by JPM global manufacturing PMI; a significant rise in liquidity has generally led to an increase in global PMI (9M lag) and vice versa.

- Hence, the sharp contraction in liquidity last year is currently pricing in a global manufacturing PMI below 50, which could result in an increase in risk aversion.

- Could the global economy surprise positively in the coming months and offset the negative forces coming from China ‘2021 tightening’, or should we expect growth expectations to fade?

- If the economic activity starts to decelerate significantly in H1 2022, then demand for risk-off assets should start to rise again and therefore limit the upside retracement in US LT bond yields.

- The bottom chart shows that a fall in the global manufacturing PMI has coincided with a consolidation in US 10Y yield in the past cycle.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok