Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

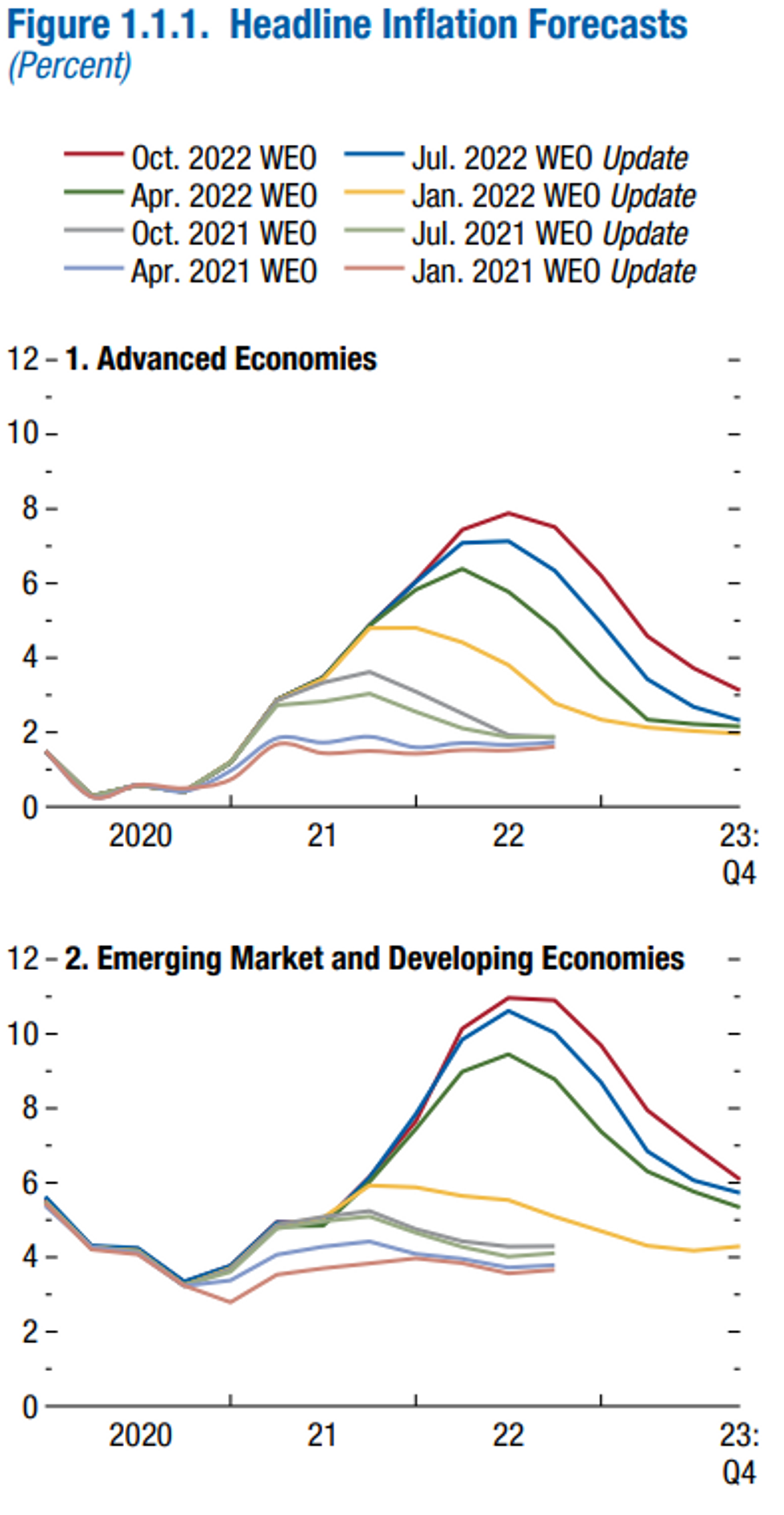

One of the most remarkable (if unsurprising) charts from the IMF's latest World Economic Outlook is from a post-mortem of their inflation projections, which continually underestimated the reality of soaring prices (as they say, "forecast errors").

- As recently as January 2022 they had expected inflation had already peaked around 5-6% and would come down across both emerging and developed countries over 2022-23. Their latest update has inflation peaking around 8% in developed markets and 11% in EM, in H2 2022. Overall 2022 annual CPI is seen at 7.2% in developed markets and 9.9% in EM.

- For what it is worth given their acknowledged prior errors, they see 2023 global developed market CPI of 4.4% (3.5% US, 5.7% eurozone, 5.1% other), and EM at 8.1% in 2023 (Asia lowest at 3.6%, EM Europe highest at 19.4%).

- The IMF cites unexpectedly buoyant demand due to fiscal stimulus, and supply side disruptions, for the forecast misses.

- Among these factors, they appear to have underestimated the steepness of the Phillips Curve slope vs very flat pre-pandemic estimates.

- That is now a common theme for central banks as they judge how far they need to tighten policy in order to sufficiently loosen the labor market to quell inflationary pressures.

Source: IMF October 2022 WEO

Source: IMF October 2022 WEO

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok