Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA

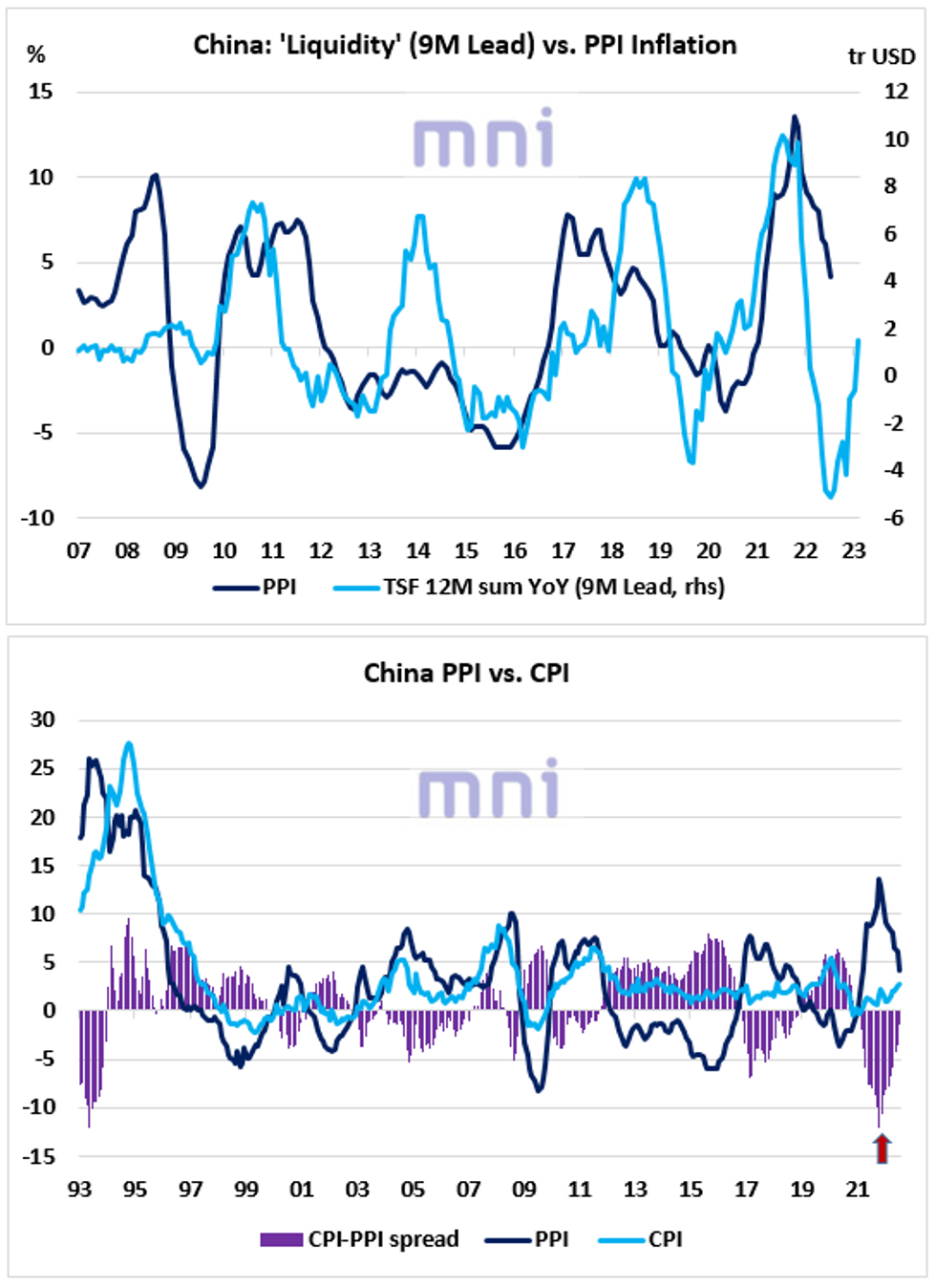

- Economic data overnight showed that inflation surprised ‘negatively’ in July, with CPI and PPI prints coming in both below analysts’ expectations.

- PPI inflation, our ‘preferred’ proxy for Chinese inflation, decelerated to 4.2% in July (vs. 4.9% exp.), down from 6.1% the previous month and now down from a 26Y high of 13.5% reached in October last year.

- In addition to the drop in commodity prices and easing supply bottlenecks, the sharp contraction in Chinese 'liquidity' last year has been pricing in a significant deceleration in inflation in 2022.

- The top chart shows that the annual change in China ‘liquidity’ has strongly led PPI inflation by 9 months in the past cycle.

- CPI inflation continued to accelerate in July, rising to a 2-year high at 2.7% (vs. 2.5% the previous month), but came in below analysts’ 2.9% expectations, with some economists speculating that headline inflation is close to a peak and will start to decelerate in the coming months.

- China Premier Li Keqiang mentioned that China can tolerate a slightly lower growth rate if inflation remains below 3.5%.

- Hence, improvements in the inflation outlook will give PBoC more room to ease to stimulate the economic activity that has been severely impacted by the zero-Covid policy.

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok