Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

We will be watchful of whether these trends are confirmed in the January PMIs (Manufacturing due Feb 2, Services Feb 5), especially after December's services PMI indicated an improvement in business activity at the time - in contrast to today's forward looking indicator.

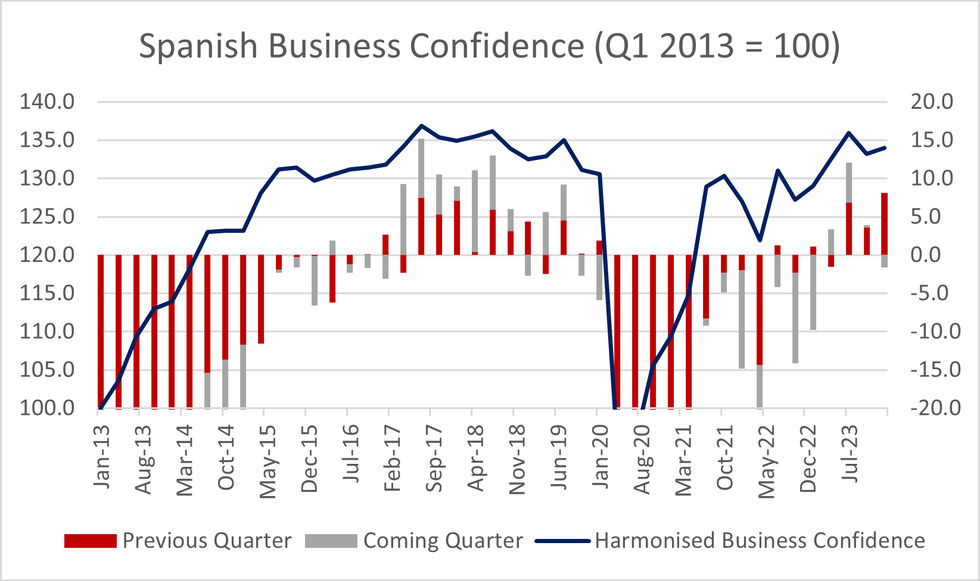

The Spanish harmonised business confidence indicator rose +0.6% to 134.0 (vs 133.2 prior) in Q1 '24, though details suggest this uptick was driven by a rise in confidence in Q4 '23, while expectations for the coming quarter fell to -1.6 (from 0.3). Increased price plans for the coming quarter suggest stagflation risks across industries.

- At a sector level, the overall confidence index rose in all sectors other than transport and accommodation. However, the forward looking assessment fell in all sectors other than industry (which remained negative at -2.3 from -2.8 prior) and construction (2.3 from 2.0 prior). Transport and accommodation saw the biggest fall, to -8.8 from -3.5 prior).

- The balances index for prices (measured as the proportion of respondents looking for price increases minus those expecting price decreases) rose for a second consecutive quarter, now at 19.9 (vs 12.0 in Q4 '23 and 8.7 in Q3 '23). All sectors other than trade saw a rise in price expectations on the quarter, with services components seeing the largest rise (possibly driven by increased wage costs, as noted in the last PMI round).

- A reminder that Spanish services CPI has remained sticky at or above 4% Y/Y since April 2022, last printing at 4.1% Y/Y in December '23.

- Employment expectations remained negative at -3.5 (vs -3.8 prior), with all subcomponents other than industry and services ex. transport and accommodation seeing falls. This is consistent with the expected employment components of the December European Commission survey.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok