Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GILTS

The well documented inflation issues in the UK are being compounded, at least in the immediate term, by the effective leadership void atop the ruling Conservative Party, with outgoing Prime Minister Boris Johnson pointing to a need for the next Prime Minister to make the choices when it comes to the next round of fiscal measures to alleviate some of the burden that UK households face at present.

- Friday’s announcement re: the latest energy price cap setting is expected to open the gates to the latest round of headwinds for UK households, with the measure set to rise comfortably above the £3,000 p/a mark from the current £1,971 p/a (after jumping from $1,277 p/a earlier this year). Meanwhile, projections suggest that the measure will sit atop $4,500 p/a after the January price cap review then comfortably above £5,000 p/a come April, at a minimum. The Russian invasion of Ukraine and related sanctions/slowing of Russian gas supply to the west is the key driver of inflation here.

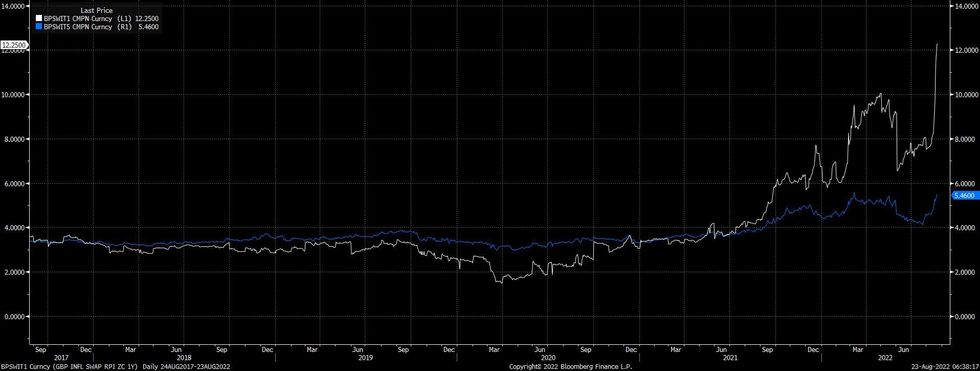

- UK 1-Year RPI zero coupon inflation swaps have registered fresh all-time highs (going back to late ’03) in recent days, with the above topics coming into greater focus and July’s UK inflation data topping expectations. The metric has topped 12%.

- A reminder that Citi suggested that CPI could peak at 18.6% Y/Y in January, also outlining the potential for the need for the BoE to hike interest rates to 6 or 7 percent in the case of deeper inflation becoming embedded in the UK. This view has got plenty of airtime in the local press over the last 24 hours.

- Note that Citi’s projections assume that the new Prime Minister will cut green levies and VAT surrounding energy bills, which will save households ~£300.

Fig. 1: UK 1- & 5-Year RPI Zero Coupon Inflation Swaps

Source:

Source:

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok