Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

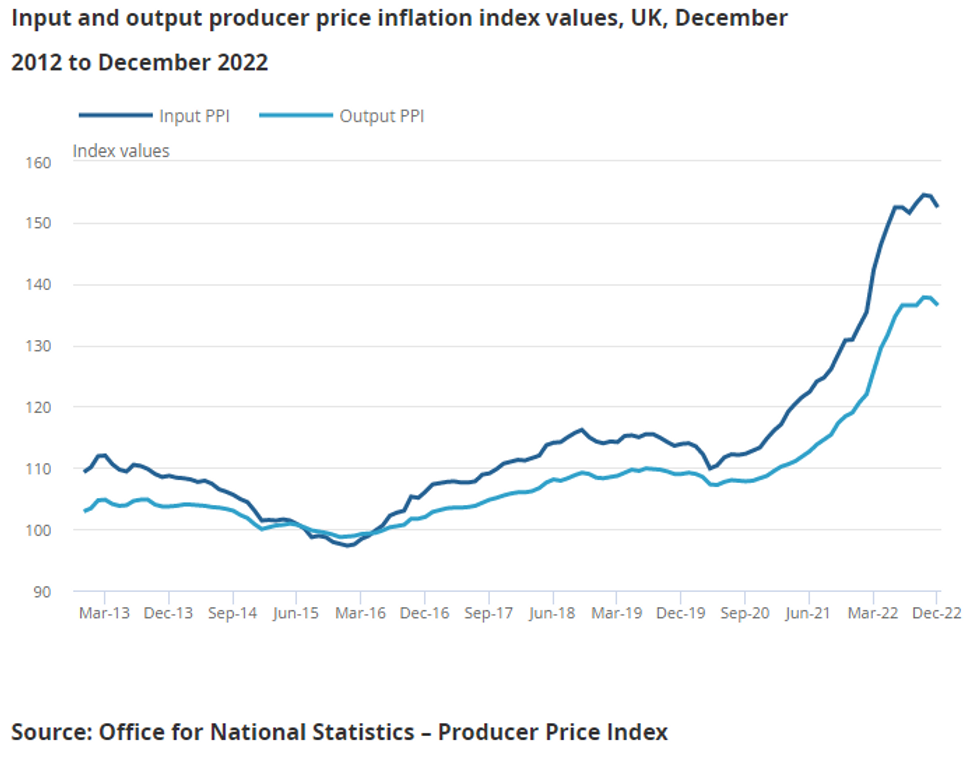

UK PPI OUTPUT DEC -0.8% M/M (FCST +0.1%), +14.7% Y/Y; NOV +16.2% Y/Y

UK PPI INPUT DEC -1.1% M/M (FCST -0.8%); +16.5% Y/Y; NOV +18.0% Y/Y

- Annualised input PPI slowed for a fifth (sixth) consecutive month in December to +16.5% y/y (output +16.5% y/y), 8.1pp below the June record high. The UK December PPI data release also included revisions, whereby rates were largely upgraded by +0.1 to +0.2pp in H2 due to reweighting corrections.

- PPI contracted by -0.8% m/m (output) and -1.1% m/m (input), the largest m/m falls since April 2020 -- the first full month post lockdowns).

- Downwards pressure came largely from crude oil, and to a lesser extent from other parts/equipment and metals. Easing supply bottlenecks alongside weakening demand is supporting slowing factory-gate inflation.

- Despite core output PPI up by +0.1% m/m, core input PPI fell by -0.4% m/m. This was the first contraction in m/m input PPI since the lockdown of April 2020. The focus will be on whether this translates into falling output PPI, which should feed into easing core CPI which had proven to be very sticky between +6.3% to +6.5% y/y since August.

- Around 45bp remain priced in for next Thursday's BOE meet.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok