Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SWEDEN

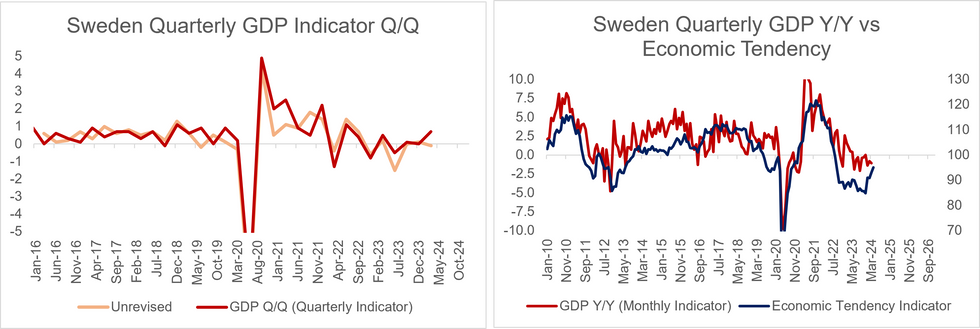

Swedish Q1 GDP saw a large upward revision relative to last month’s flash estimate, printing at 0.7% Q/Q (vs 0.0% cons, -0.1% flash) and 0.7% Y/Y (vs -0.9% cons, -1.1% flash).

- The flash GDP indicator is often revised – sometimes heavily – but the extent of this revision is still surprising. Analysts had expected a much more modest upward revision following the March monthly activity data, where GDP was positive on a sequential basis.

- Since Q1 2016, the average absolute error of the flash estimate (vs the final) has been 0.5pp, below Q1 2024’s 0.8pp.

- The press release notes that the largest contribution to the Q/Q growth reading came from changes in inventories at 0.5pp – traditionally a volatile category.

- Final domestic demand (i.e. private consumption, public consumption and gross fixed capital formation) contributed just 0.1pp, with net exports contributing the remaining 0.1pp (exports 0.1pp, imports 0.0pp).

- As such, a “cleaner” read of first quarter GDP suggests that activity remains relatively muted, though has recovered from the last few year’s lows.

- The Riksbank’s March MPR forecast was 0.0% Q/Q and -0.9% Y/Y, so today’s stronger-than-expected reading (even when excluding inventories) should confirm the case for holding rates in June, in line with recent Executive Board communications.

- Employed persons and hours worked both fell 0.1% Q/Q, meaning labour productivity rose 0.9% Q/Q (though again, the inventory effect will have boosted this reading artificially).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok