Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SOUTH KOREA

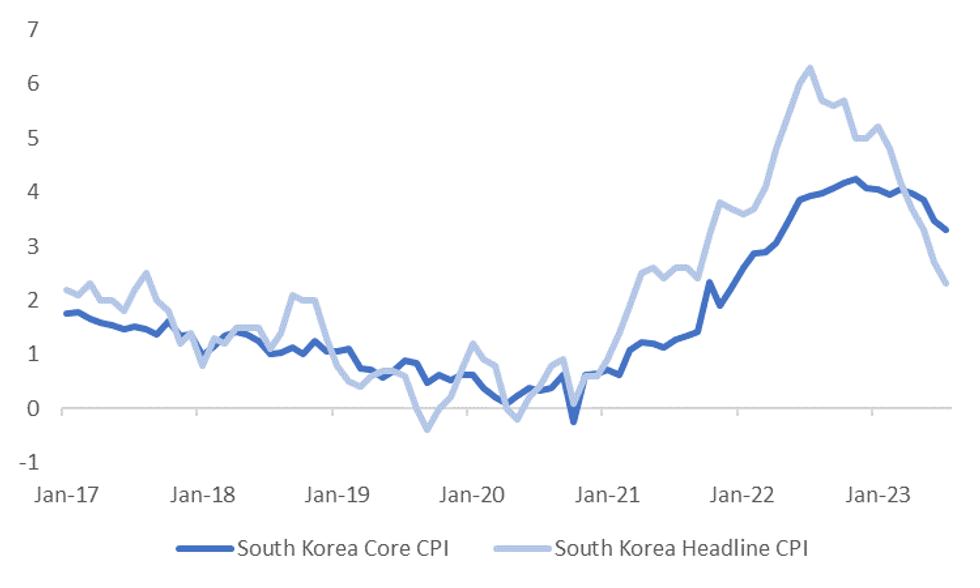

South Korea July CPI was weaker than expected, albeit at the margins. The headline was +0.1% m/m, versus +0.2% forecast, the prior outcome was flat. in y/y terms, we came in at 2.3%, against a 2.4% forecast and 2.7% prior. The core came in at 3.3% y/y, versus 3.5% prior. There is no consensus for this outcome.

- Headline CPI y/y momentum continues to retreat, we are now back to levels that prevailed in the first half of 2021. The authorities are also likely to be pleased with the continued move down in core CPI y/y momentum, see the chart below.

- Still, base effects become less favorable as we progress forward, with the y/y headline pace peaking in July last year. The BoK has stated headline inflation momentum may pick up in August. So, today's result may not shift their thinking around the policy outlook. The core measure didn't peak until November last year though.

- Looking at the detail, weaker housing/utilities (-1.3% m/m) offset a rebound in food prices (+0.8% m/m). Transport prices also edged higher (+0.4% m/m), as did restaurants/hotels (+0.5% m/m). 7 out of the 12 sub-indices for inflation recorded higher m/m outcomes relative to June.

Fig 1: South Korea Inflation - Headline & Core Y/Y

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok